EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It measures operational performance by removing non-operational and non-cash expenses, giving investors, lenders, and business owners a clean view of how well the core business performs.

Key Takeaways

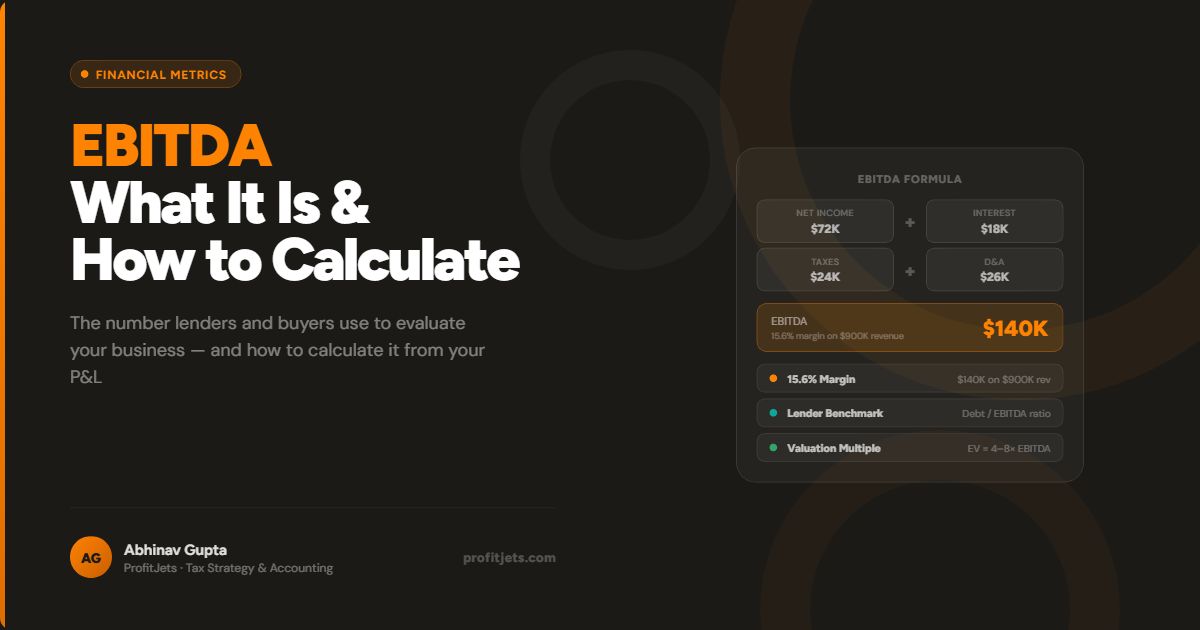

- EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization. It is the most widely used metric in M&A and lending contexts.

- On $1M revenue with $275K EBITDA, the EBITDA margin is 27.5% — a strong benchmark for most industries.

- EBITDA is not the same as cash flow. It excludes working capital changes and capital expenditures.

- EBITDA can be negative — when operating expenses exceed gross income, which is a signal that requires immediate investigation.

EBITDA is one of the most discussed financial metrics in business — and one of the most misunderstood. Venture capitalists, private equity firms, and banks rely on it precisely because it removes the variables that differ from company to company (how they are financed, where they are incorporated, what depreciation method they use) and isolates the one thing they want to compare: operational performance.

For small business owners, understanding EBITDA matters most when you are raising capital, applying for a loan, benchmarking against peers, or preparing for a potential acquisition or exit.

What Is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a financial metric that measures operational performance by excluding non-operational and non-cash expenses from the bottom line.

- Interest is excluded because it reflects financing decisions, not operational performance. Two identical businesses with different debt loads would show different net incomes but the same EBITDA.

- Taxes are excluded because tax rates vary by location and structure — removing them allows comparison across geographies and entity types.

- Depreciation and amortization are non-cash charges that reduce net income but do not affect the cash generated by operations during the period.

Why Is EBITDA Important?

EBITDA is important for four core reasons:

- It removes financial distortions from interest and depreciation/amortization charges, producing a cleaner operating result

- It enables comparable analysis across different industries and company sizes

- It highlights operational efficiency separate from financing and tax decisions

- It is widely used by venture capitalists, private equity firms, and banks as a basis for valuation multiples and loan covenants

Investors use EBITDA because it shows how well a company performs operationally, without distortion from tax jurisdictions or capital structure choices. It makes a company in Delaware directly comparable to one in Texas, and a debt-heavy business comparable to a debt-free one.

How to Calculate EBITDA

The formula is:

Net Income: $200,000

Interest: $15,000

Taxes: $30,000

Depreciation: $20,000

Amortization: $10,000

EBITDA = $275,000

| Component | Amount | Why it is added back |

|---|---|---|

| Net Income | $200,000 | Starting point |

| Interest | $15,000 | Financing decision, not operations |

| Taxes | $30,000 | Varies by location and structure |

| Depreciation | $20,000 | Non-cash charge on fixed assets |

| Amortization | $10,000 | Non-cash charge on intangibles |

| EBITDA | $275,000 | Clean operational earnings |

EBITDA Margin

EBITDA margin expresses EBITDA as a percentage of revenue, making it comparable across companies of different sizes:

Using the example above with $1,000,000 in revenue: $275,000 / $1,000,000 x 100 = 27.5% EBITDA margin. This is a strong result for most industries and signals efficient operational management.

Three levers drive EBITDA margin improvement: increasing revenue (ideally without proportional cost growth), reducing operating expenses, and optimizing pricing to improve contribution margin on each sale.

How to Find EBITDA on Financial Statements

EBITDA does not appear as a line item on standard financial statements because it is a non-GAAP metric. You calculate it from data that does appear:

- Start with net income from the income statement

- Locate interest expense on the income statement (usually in the “other income/expense” section)

- Find income tax expense on the income statement

- Get depreciation and amortization from the footnotes or the cash flow statement (it appears as a non-cash add-back in operating activities)

- Add all four components to net income

EBITDA vs. Other Profit Metrics

| Metric | Definition | Primary Use Case |

|---|---|---|

| Net Income | Bottom-line profit after all expenses | Final profit for tax or dividend decisions |

| Gross Profit | Revenue minus COGS | Production and sourcing efficiency |

| Operating Profit | Gross profit minus operating expenses | Core business profitability before financing |

| EBITDA | Earnings before interest, taxes, D&A | Clean operational view; M&A and lending basis |

Limitations of EBITDA

EBITDA is powerful but has three significant limitations that every user should understand:

- Ignores debt burden. A company with $5M in debt and $500K in annual interest payments looks identical to a debt-free company at the EBITDA line. That difference matters enormously for actual financial health.

- Excludes capital expenditures. Asset-heavy businesses (manufacturers, trucking companies, hospitals) need ongoing capex just to maintain operations. Ignoring this makes EBITDA a misleading proxy for cash generation in those industries.

- Subject to manipulation. Because it is non-GAAP, companies have flexibility in what they classify as one-time items to be excluded. Always review the adjustments that were made to arrive at “adjusted EBITDA.”

EBITDA excludes working capital changes and capital expenditures. A business can have strong EBITDA while consuming cash due to inventory build, slow receivables, or heavy investment spending. Always review free cash flow alongside EBITDA for a complete picture.

When Small Businesses Should Use EBITDA

EBITDA is most useful for small businesses in four specific situations:

- Preparing reports for investors or lenders. Banks and investors expect EBITDA when evaluating creditworthiness or valuation. Not knowing your EBITDA puts you at a disadvantage in those conversations.

- Benchmarking internal performance. Track EBITDA quarter over quarter to see whether operational efficiency is improving, independent of financing or tax changes.

- Comparing operational efficiency. If you are evaluating an acquisition target or comparing yourself to a competitor, EBITDA provides the most apples-to-apples view of operating performance.

- During mergers, acquisitions, or exit planning. Business valuations are frequently expressed as a multiple of EBITDA (e.g., “8x EBITDA”). Knowing your number and how to improve it is foundational to exit planning.

Even if you are pre-profit, track EBITDA from your first full quarter of operation. It creates a baseline for the trajectory conversation lenders and investors will want to have, and it signals financial sophistication that builds credibility.

Need help calculating your EBITDA and preparing investor-ready financial statements?

Talk to a ProfitJets AdvisorFrequently Asked Questions

Is EBITDA the same as cash flow?

Why do investors focus on EBITDA rather than net income?

How can I improve my EBITDA margin?

Can EBITDA be negative?

Should small businesses track EBITDA?

Ready to track EBITDA accurately and use it to prepare for your next funding round or lender conversation?

Schedule a Free ConsultationProfitJets Editorial Team

The ProfitJets team writes practical finance guides for small and mid-sized business owners navigating growth, reporting, and strategic decisions.