Businesses that sell things must take into consideration the worth of these products when filing their income taxes. The IRS has recognized a number of methods for valuing your inventory.

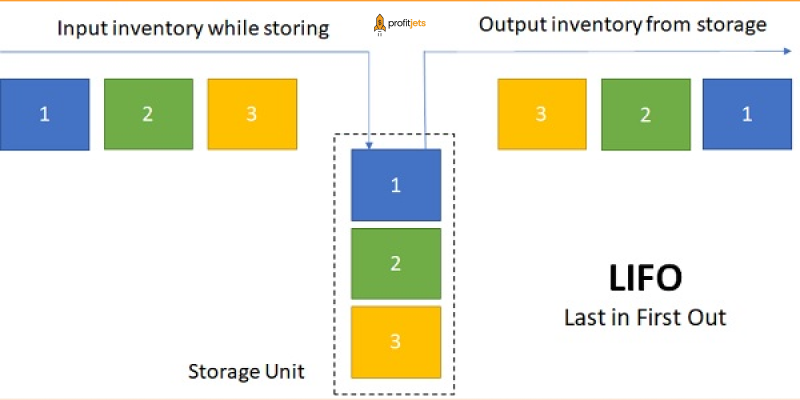

One of these inventory valuation methods is last in, first out (LIFO). It is presumptive that during an accounting year, the first products sold are those that were last added to inventory.

Now let’s look at LIFO, which stands for last in, first out in brief.

What is LIFO, Or Last-In, First-Out?

The Last-in, First-out (LIFO) is a technique of inventory valuation that is predicated on the idea that the last-produced or last-bought assets will be the ones to incur expenses. In other words, the most recent things produced or purchased are withdrawn and expensed according to the last-in, first-out method. As a result, the newest inventory expenses are expensed first while the older costs remain on the balance sheet.

Retailers and auto dealerships are typical examples of businesses adopting LIFO inventory values because they can benefit from lower taxes (when prices rise) and better cash flows.

However, many businesses prefer to utilize FIFO since, if a company uses a LIFO valuation when filing taxes, it must also use a LIFO valuation when reporting financial results to shareholders, which reduces net income and, ultimately, earnings per share.

Relation Between Inflation, Net Income, And Last In, First Out (LIFO):

")

The outcomes of the three inventory-costing techniques are the same when there is no inflation. However, the choice of accounting system might significantly impact valuation ratios if Inflation is substantial. As a result, the effects of FIFO, LIFO, and average cost vary:

Although FIFO boosts net income since COGS are valued using inventory that may be several years old, it also gives a better representation of the value of ending inventory (on the balance sheet). Increased net income may sound fantastic, but it can also result in more taxes due from the business.

Due to the possibility of understating inventory value, LIFO is not a reliable indicator of ending inventory value. Due to increasing COGS, LIFO leads to reduced net income (and taxes). However, under LIFO during Inflation, there are fewer inventory write-downs.

Results from average cost are in the middle of FIFO and LIFO. If prices fall, the exact reverse of what was stated above will be accurate.

Methods for Inventory Valuation:

Your firm’s stock of goods, components, and supplies is a valuable asset. Additionally, the prices related to creating, purchasing, managing, and delivering inventory are crucial business costs. Therefore, you need the means to identify the objects in your stock and give them a value before you can value them.

How to Determine the Cost of Goods Sold (COGS):

The cost of goods sold (COGS) for a firm is calculated through the inventory process at the end of the year and is reported on your business tax return. Your gross profit for the year is calculated by subtracting COGS from your gross receipts (before expenses).

Here’s how COGS are determined:

- Inventory count at the start of the year.

- Including the cost of products, labor, and other expenses.

- Removing inventories at the year’s end.

LIFO Inventory Costing: How It Operates

There are various ways to calculate the cost of your inventory when performing the COGS calculation. There are three typical methods for valuing stock:

1. Specific Identification:

When you can identify and correlate the goods’ actual costs to their costs, specific identification is employed for certain types of inventory (for example, a car using the Vehicle ID Number).

2. LIFO:

The LIFO system operates under the premise that you sell, consume, or dispose of the objects you purchase.

3. First In, First Out (FIFO):

First In, First Out (FIFO), the FIFO technique, assumes that the goods you have as the business owner bought or created first are the goods you sell, eat, or discard.

If you use the LIFO cost method, you can use one of the IRS-approved grouping criteria to make it simpler to count the items. Two of these guidelines for LIFO valuation are:

- The classification of goods and products into classes according to their types using the dollar-value technique.

- The condensed dollar-value approach, with numerous inventory classifications divided into broad groups.

What Benefits Does First In, First Out (FIFO) Have?

Have")

The most evident benefit of FIFO is that it is the most popular technique of inventory valuation internationally. It is also the most precise way to match the actual flow of goods with the predicted flow of costs, giving organizations a more accurate picture of the costs associated with inventory. Anticipating that the price of buying fresh inventory will be higher than the price of buying older stock also lessens the impact of Inflation. Finally, it facilitates inventory obsolescence.

Choosing the LIFO Approach:

The LIFO method must be chosen if you want to utilize it; FIFO inventory costing is the default. Additionally, once you switch to the LIFO approach, you can’t revert to FIFO without the IRS’s permission.

To switch to LIFO, you must fill out and submit an application. Submit the form along with your tax return for the year you begin using LIFO.

In order to complete the application, you must ensure the following:

- Indicate which goods will be subject to the LIFO mechanism.

- Specify and explain the inventory method(s) you employed to value these items in the previous year.

- Describe the products for which the LIFO technique WILL NOT be applied.

Conclusion:

So, to summarize, we can say that one inventory method used to calculate the cost of inventory for the cost of goods sold is LIFO (Last-In, First-Out). Contrary to LIFO valuation, which assumes the earliest inventory items are sold first, LIFO valuation assumes the last things in inventory are sold first.

So, if you also want to get services related to inventory, then Profit Jets is just a perfect option for you. Profit Jets provides you with specialized accounting, bookkeeping, tax, and advising solutions to assist your company in adhering to all legal requirements and achieving your objectives. So, now, what are you waiting for? Contact Profit Jets today.