IRS Form 4562 (Depreciation and Amortization) is used by businesses to report:

- Depreciation of business assets

- Section 179 expense deductions

- Bonus depreciation claims

- Amortization of startup costs and other intangibles

Table of Contents

Who Must File Form 4562?

You need to complete this form if you:

- Placed business property into service during the tax year

- Claim Section 179 expensing

- Are deducting vehicle expenses using actual costs

- Need to report amortization of organizational costs

- Claim special depreciation allowances

Important: Even if you don’t have current-year depreciation, you may need to file if claiming Section 179. Professional tax services can determine your requirements.

Step-by-Step Guide to Completing Form 4562

Step 1: Identify Depreciable Assets

Gather records for all business assets, including:

- Purchase dates and costs

- In-service dates

- Asset classifications (5-year, 7-year property, etc.)

- Prior depreciation schedules

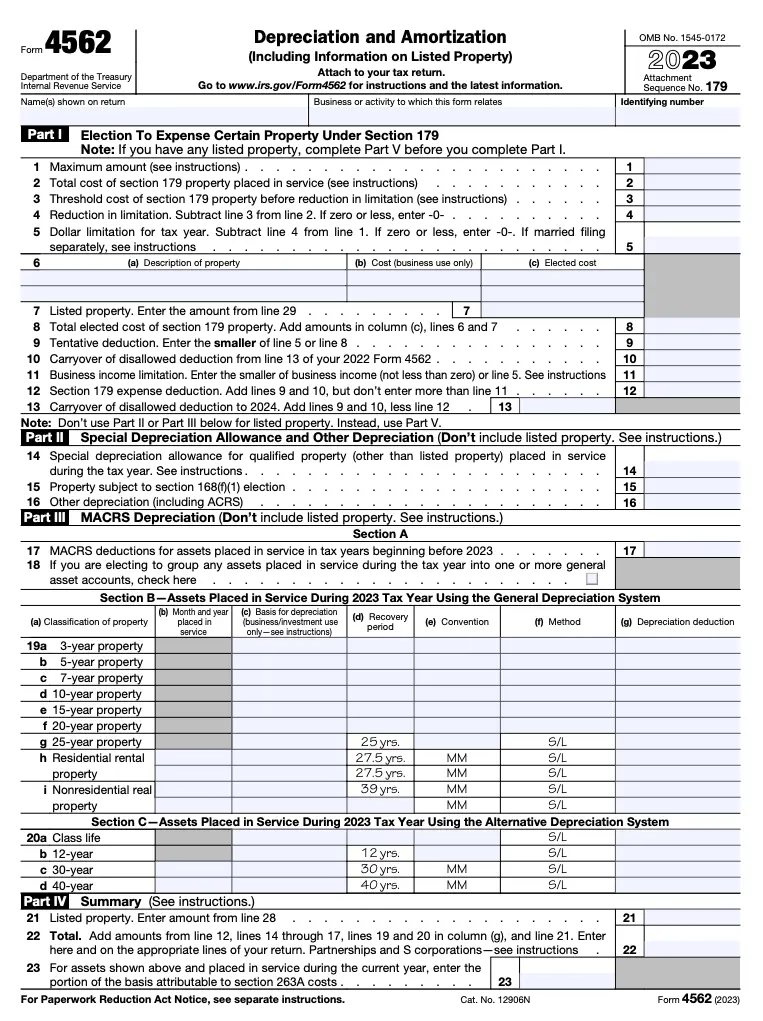

Step 2: Complete Part I – Election to Expense Certain Property

For Section 179 deductions:

- Line 1: Maximum allowable deduction ($1,160,000 for 2023)

- Line 2: Total cost of qualifying property

- Line 5: Calculate your Section 179 deduction

- Line 6: List property descriptions and costs

Note: Review Form 4562 instructions for special rules on SUVs and other limitations.

Step 3: Complete Part II – Special Depreciation Allowance

For bonus depreciation:

- Line 14: Qualifying property placed in service

- Line 15: Calculate 80% bonus depreciation (2023 rate)

- Line 16: List property descriptions

Step 4: Complete Part III – MACRS Depreciation

For regular depreciation:

- Line 19: List asset classes and depreciation methods

- Line 20: Calculate depreciation for each asset

- Line 22: Total current year depreciation

Tip: Reconcile with your financial statements for accuracy.

Step 5: Complete Part IV – Summary

- Line 24: Total all depreciation amounts

- Line 25: Include on appropriate business tax return line

Step 6: Complete Part V – Listed Property

For vehicles, computers, etc.:

- Line 26: Business use percentage

- Line 27: Expense allocation

- Line 28: Depreciation calculation

Step 7: Complete Part VI – Amortization

For organizational costs and other intangibles:

- Line 42: Description of amortized items

- Line 43: Amortization period

- Line 44: Current year deduction

Common Mistakes to Avoid

- Missing asset in-service dates – Critical for depreciation start

- Incorrect asset classifications – 3-year vs 5-year property etc.

- Miscalculating business use percentages – Especially for vehicles

- Overlooking bonus depreciation changes – Rates change annually

- Failing to reconcile with financial statements – Must match book records

For complex asset portfolios, professional tax services ensure proper reporting.

Advanced Reporting Considerations

Financial Statement Reconciliation

- Compare tax vs. book depreciation

- Track deferred tax liabilities

- Document Section 179 carryforwards

Special Situations

- Like-kind exchange adjustments

- Asset dispositions and recapture

- Improvement vs. repair classifications

- Change in accounting methods

State Compliance

- Varying state rules on bonus depreciation

- Different Section 179 limits

- Addback requirements

Final Thoughts

Proper completion of IRS Form 4562 is essential for accurate reporting of business asset depreciation and amortization. By maintaining detailed asset records, reconciling with financial statements, and carefully following the latest Form 4562 instructions, businesses can maximize legitimate deductions while remaining compliant. For companies with significant capital expenditures, frequent asset acquisitions, or complex depreciation scenarios, partnering with professional tax services provides the expertise needed to navigate these technical requirements efficiently.