Bookkeeping for small businesses is the foundation of sound financial management. Whether you’re launching a new venture or managing a growing company, tracking your finances ensures smarter decisions and long-term success.

If you’re a small business owner, managing the books can feel overwhelming—but it doesn’t have to be. In this blog, we’ll walk through 10 simple and essential bookkeeping examples that every small business can implement easily.

Table of Contents

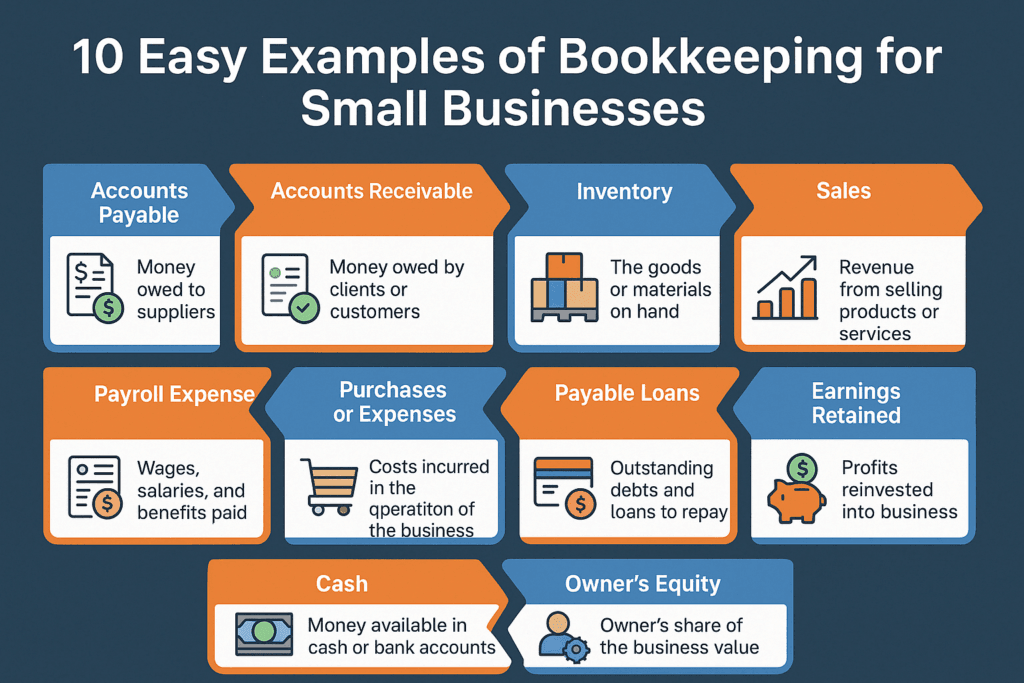

1. Accounts Payable

Definition: Money your business owes to vendors for goods or services received.

Example: You receive raw materials from a supplier with a 30-day payment term. Recording this as an accounts payable entry ensures it’s paid on time and tracked in your balance sheet.

2. Accounts Receivable

Definition: Money owed to your business by customers.

Example: You provide services on credit and send an invoice. The unpaid invoice becomes an accounts receivable item until it’s collected.

3. Inventory Tracking

Definition: The value of goods you hold for sale.

Example: You purchase 500 units of product. Record the cost and track the quantity sold or unsold regularly to assess inventory turnover and investment.

4. Sales Records

Definition: Income generated from selling goods or services.

Example: Every customer purchase—whether online or in-store—should be recorded. This forms the base of your income reports and revenue projections.

5. Payroll Expenses

Definition: Wages, salaries, and benefits paid to employees.

Example: Monthly payroll costs, including taxes and insurance, should be recorded under payroll expenses in your general ledger.

6. Purchases & Expenditures

Definition: Money spent on business operations.

Example: Office supplies, software subscriptions, or production materials fall under this category. Keeping a log of these helps with budgeting and tax deductions.

7. Loans Payable

Definition: Any borrowed funds that must be repaid.

Example: If you take a business loan to fund equipment, record the loan amount and monthly repayments, including interest.

8. Retained Earnings

Definition: Net income retained in the business rather than distributed as dividends.

Example: If your business earns a profit and you decide to reinvest it, this amount is recorded as retained earnings, reflecting business growth over time.

9. Cash Flow Monitoring

Definition: Tracking actual cash moving in and out.

Example: Daily expenses paid in cash, ATM withdrawals, and petty cash payments need to be recorded for a clear view of available liquidity.

10. Owner’s Equity

Definition: Capital invested by the owner(s) in the business.

Example: If you invest $10,000 of your personal funds into the business, record it under owner’s equity. This helps measure how much value the owner holds in the company.

Final Thoughts

Bookkeeping for small businesses doesn’t have to be complicated. With these 10 easy-to-follow examples, small business owners can gain control over their finances and make more informed decisions.

📞Need help managing your books? Contact Profitjets for professional bookkeeping and financial solutions tailored for your business.

Frequently Asked Questions

1. What are basic bookkeeping tasks for small businesses?

Basic bookkeeping includes recording transactions, tracking income and expenses, reconciling accounts, managing invoices, and preparing financial statements.

2. Why is bookkeeping for small businesses is important?

Bookkeeping helps small business owners understand their financial health, meet tax obligations, make data-driven decisions, and avoid cash flow issues.

3. What’s the difference between accounting and bookkeeping?

Bookkeeping involves recording financial data daily, while accounting includes interpreting that data to provide insights and prepare reports.

4. Can small business owners do bookkeeping themselves?

Yes, many use tools like QuickBooks, Xero, or FreshBooks. However, outsourcing bookkeeping ensures accuracy and frees up time to focus on growth.

5. How often should I update my bookkeeping records?

Consistent updates prevent errors, reduce stress during tax season, and give real-time financial visibility.