Is Your DSO (Days Sales Outstanding) Silently Killing Your Cash Flow

Your Days Sales Outstanding is a direct report of how effectively your business converts revenue into usable cash. Businesses that monitor DSO consistently are better

Your Days Sales Outstanding is a direct report of how effectively your business converts revenue into usable cash. Businesses that monitor DSO consistently are better

The current ratio and quick ratio are the two most important liquidity metrics every business owner should track. While profits can look healthy on paper,

Most business owners find out their debt-to-equity ratio matters at exactly the wrong moment, when a lender declines their loan application or an investor asks

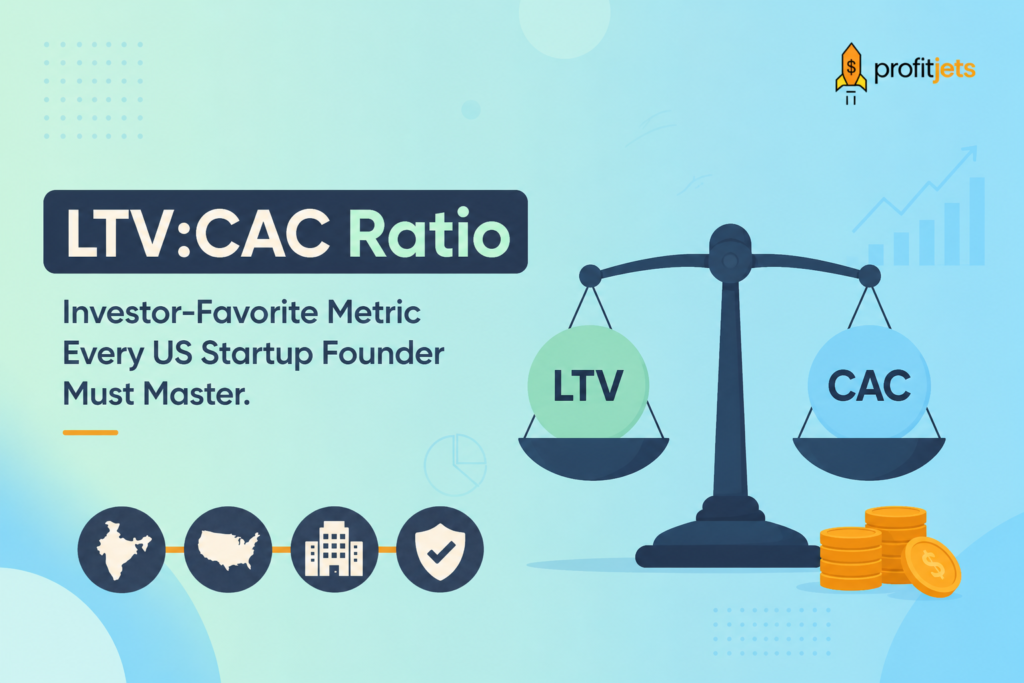

The LTV:CAC (Lifetime Value to Customer Acquisition Cost) ratio is one of the most important metrics for understanding whether your business is truly growing or

Recent studies indicate that Customer acquisition costs have risen drastically in the last two years. Paid channels are saturated. Ad platforms are squeezed. And yet,

Working capital is the money a business has available to run its day-to-day operations. It’s what’s left after subtracting current bills and expenses from current