Overview

As defined by the Internal Revenue Service, the IRS Form 5329 is used to report and calculate additional taxes (penalties) on your individual retirement accounts (IRAs), qualified retirement plans, and other tax-benefited savings. It also includes your health (HSAs) and educational savings accounts (ESAs).

Current Updates and Developments: IRS Form 5329

The latest IRS guidance (updated as of 2026) continues to position Form 5329 as a key compliance tool for reporting penalties related to early withdrawals, excess contributions, and missed required minimum distributions (RMDs).

Understanding IRS Form 5329 is essential because it applies to every individual who might owe a penalty, and for married couples who are filing jointly, each spouse should submit their IRS Form 5329 individually.

Beyond reporting penalties, Form 5329 is used to identify exceptions and potentially reduce or eliminate them.

About IRS Form 5329

The IRS Form 5329 is a tax form usually filed along with your return (which is Form 1040) to report the penalty tax waivers related to retirement and savings accounts.

This applies to:

- Traditional and Roth IRAs,

- 401(k) and similar retirement plans,

- Health Savings Accounts (HSAs),

- Education savings accounts (ESAs) and

- ABLE accounts.

Need expert guidance on IRS Form 5329 or tax compliance?

Simplify your tax filing queries with ProfitJets.

How to recover your additional taxes

We are all aware that we should be saving up more for the uncertain job markets and secured retirement benefits.

But what if you contribute more than the standard annual limit to your health savings account (HSA) or your retirement plans? Or when you withdraw funds earlier than permitted from your education savings account (ESA)? Or even missing your required minimum withdrawals (RMDs), where you’re supposed to take money out of your retirement account but don’t do it on time.

In the above cases, IRS Form 5329 is used to recover and analyze your IRS penalties from the unforeseen situations by requesting a penalty waiver.

But how do these penalties occur?

Mostly in situations when,

- You’re trying to withdraw your funds too early.

- You have contributed more than the set limit.

- You have failed to take your required minimum withdrawals (RMDs).

Types of Penalties Reported on IRS Form 5329

As per IRS guidelines, Form 5329 calculates penalties under IRC §72(t), §4973, and §4971, regulated to protect retirement savings while allowing legitimate exceptions.

IRS Form 5329: Excess Contributions (Tax Year 2026)

According to federal norms, various tax-advantaged accounts such as IRAs, 401(k)s, HSAs, ESAs, and ABLE accounts have annual contribution limits set by the Internal Revenue Service, with catch-up contributions allowed for older individuals.

For the 2026 tax year, the contribution limits set by IRS are

Exceeding these standardized limits results in additional taxes reported using Form 5329.

Why This Matters

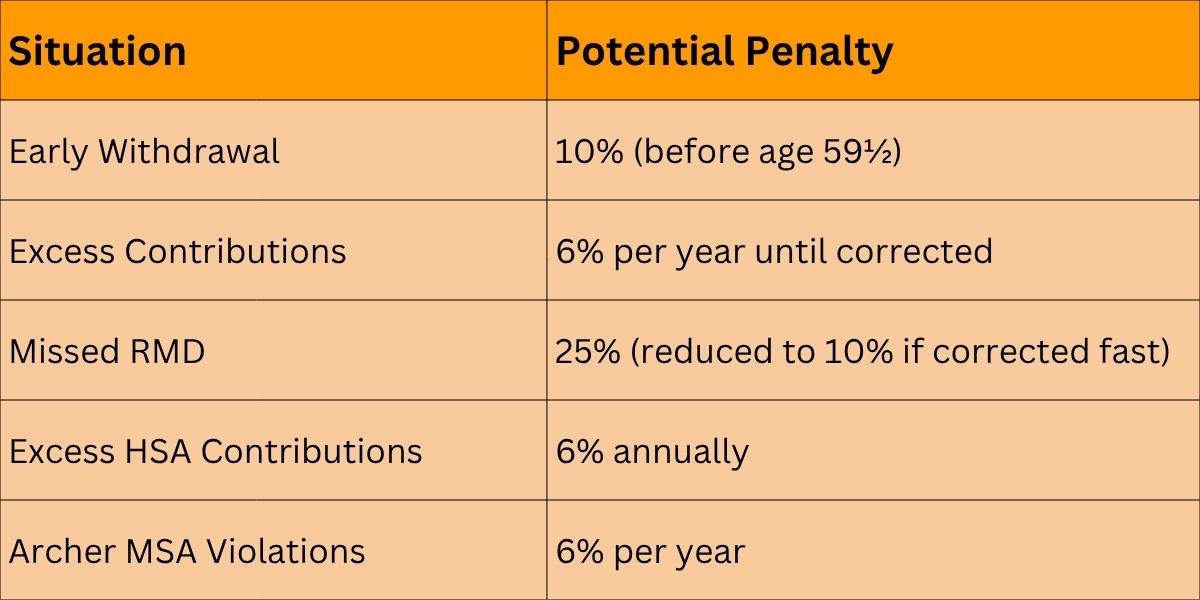

When you are contributing more than these limits by the IRS, it can result in a 6% penalty per year until the excess amount is corrected. Closely monitoring your contributions is essential to avoid such unnecessary constraints.

When Do You Need to File IRS Form 5329?

In today’s complex tax environment, even small oversights in managing tax-advantaged accounts can result in additional penalties. IRS Form 5329

becomes relevant when these rules are not followed, helping taxpayers report, review, and in some cases reduce these penalties.

1. Early Withdrawals from Retirement Accounts

When you withdraw early before age 59½, it may result in a 10% additional tax, unless you qualify for specific exceptions such as medical expenses, disability, or a first-time home purchase.

2. Excess Contributions

Contributing more than the allowed limit to IRAs, HSAs, or other eligible accounts can result in a 6% penalty per year, which continues until the excess amount is corrected.

This is one of the most common yet overlooked triggers, especially among individuals managing multiple income streams.

3. Missed Required Minimum Distributions (RMDs)

Failing to withdraw the required amount from retirement accounts may lead to penalties ranging from 10% to 25%, depending on how quickly the error is corrected.

This typically impacts retirees and account holders who are unaware of changing RMD rules.

4. Violations in Other Tax-Advantaged Accounts

Errors in managing other savings vehicles can also require filing Form 5329. These include:

- Coverdell Education Savings Accounts (ESAs),

- ABLE accounts,

- Health Savings Accounts (HSAs) and

- Archer Medical Savings Accounts (MSAs).

Need expert guidance on IRS Form 5329 or tax compliance?

Simplify your tax filing queries with ProfitJets.

Additional Situations Where IRS Form 5329 May Apply

Beyond the common scenarios, taxpayers may also need to file Form 5329 in the following cases:

- Failure to correct excess contributions on time, leading to recurring penalties

- Incorrect reporting of distributions on Form 1099-R

- Taking non-qualified distributions from education or health savings accounts

- Filing an amended return to report missed penalties or claim exceptions

- Requesting a waiver for penalties, particularly in cases of reasonable error (such as missed RMDs)

Penalty Waivers (RMD Cases)

The IRS may waive penalties if:

- The failure was due to reasonable error and

- You are taking steps to correct it.

Taxpayers must file Form 5329 and include a clear explanation when requesting a waiver.

Where common exceptions include first-time home purchase, qualified education expenses, disability or death, and high medical expenses.

How IRS Form 5329 Fits into Your Tax Filing

- Typically filed with your annual return (Form 1040)

- Can be filed separately if missed earlier

- Required even if no regular income tax is owed

Things You Should Avoid Doing Right Away

As per IRS guidelines, failure to file this IRS Form 5329 when required can result in additional penalties.

- ❌When you owe penalties and you’re not complying with Form 5329, you will be charged extra.

- ❌Please stop contributing more than the IRS regulated limit.

- ❌Do not miss your RMD due dates.

- ❌Not claiming exceptions that you are eligible for.

- ❌Filing without looking over the supporting documents.

Final Thoughts

IRS Form 5329 plays a critical role in managing additional tax liabilities tied to retirement and other tax-advantaged accounts. Understanding when and how to file Form 5329 can help you avoid unnecessary penalties, stay compliant with IRS regulations, and make informed financial decisions.

Whether it’s early withdrawals, excess contributions, or missed required minimum distributions (RMDs), addressing these issues proactively can prevent long-term financial impact.

At ProfitJets, we specialize in helping individuals, freelancers, and businesses navigate complex U.S. tax requirements with clarity and precision, ensuring accurate filings and optimized outcomes.

Need expert guidance on Form 5329 or tax compliance?

Simplify your tax filing queries with ProfitJets.

Commonly Asked Questions (FAQs)

Q1. What happens if I discover I made excess contributions to my retirement account after filing my tax return?

Withdraw excess contributions as soon as possible and file Form 5329 with your amended return to minimize penalties and interest. It’s much easier to correct the error proactively than to deal with accumulated penalties over multiple years.

Q2. Do I need to file Form 5329 every year?

No. Form 5329 is required only in years where a taxpayer incurs additional taxes or needs to claim an applicable exception or waiver.

Q3. Can penalties reported on Form 5329 be waived?

Yes. The IRS may grant penalty relief in specific circumstances, most notably for missed RMDs. Provided the taxpayer can demonstrate reasonable cause and has taken timely corrective action. A detailed explanation must accompany the filing.

Q4. Can I file Form 5329 separately?

Yes. Form 5329 may be filed as a standalone submission, particularly in cases where it was omitted from the original return or when reporting prior-year corrections.

Q5. What are the consequences of not filing Form 5329?

Failure to file Form 5329 when required may result in continued assessment of penalties and interest. Additionally, the statute of limitations may remain open, exposing the taxpayer to prolonged compliance risk.

Q6. Do I need to file Form 5329 if I took an early withdrawal but qualify for an exception?

Yes. Even if you qualify for an exception (disability, medical expenses, first-time home purchase, etc.), you must file Form 5329 to claim the exception and avoid the 10% early withdrawal penalty.