IRS Form 1041 (U.S. Income Tax Return for Estates and Trusts) is the primary tax document for:

- Revocable and irrevocable trusts

- Estates of deceased persons

- Bankruptcy estates

- Other fiduciary entities

Table of Contents

Who Must File Form 1041?

Filing is required if the entity:

- Has gross income ≥ $600

- Has any taxable income

- Has a beneficiary who is a nonresident alien

- Is required to file under specific trust terms

Important: Even if not required, filing may be beneficial. Professional tax services can assess your specific situation.

Step-by-Step Guide to Completing Form 1041

Step 1: Determine Filing Requirements

Review:

- Trust or estate governing documents

- Current year income and deductions

- Beneficiary distribution requirements

- State filing obligations

Step 2: Gather Required Documentation

Prepare:

- Trust agreement or will

- Prior year tax returns

- Financial statements for the entity

- K-1 forms for beneficiaries

- Expense receipts and income statements

Step 3: Complete Basic Information Section

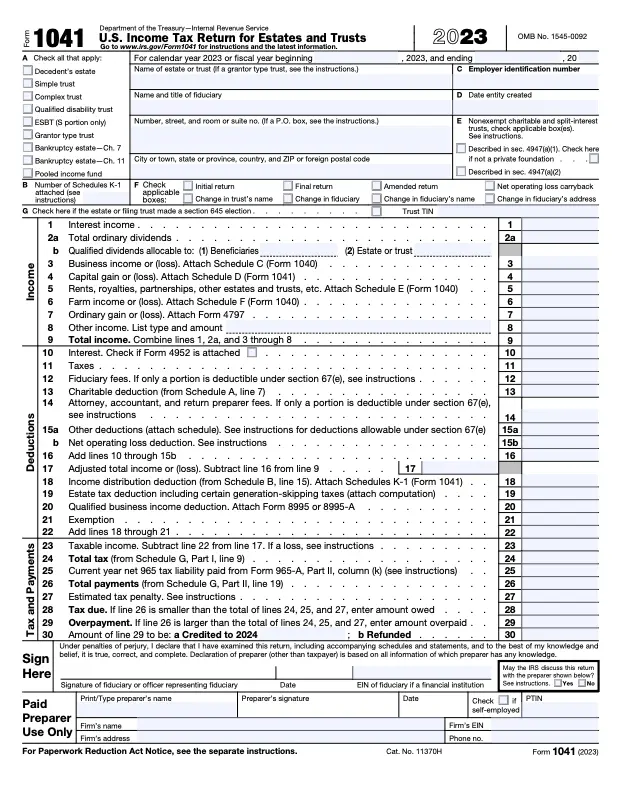

- Line 1a: Estate/trust name and EIN

- Line 1b: Fiduciary’s name and address

- Line 1c: Date entity was established

- Line 1d: Date entity terminated (if applicable)

Step 4: Report Income (Page 1)

- Line 2: Interest income

- Line 3: Dividends

- Line 4: Business income/loss

- Line 5: Capital gains/losses

- Line 6: Other income

Step 5: Claim Deductions (Page 1)

- Line 9: Fiduciary fees

- Line 10: Charitable deductions

- Line 11: Tax preparation fees

- Line 12: Other deductions

Step 6: Complete Tax Computation (Page 2)

- Line 22: Taxable income

- Line 23: Tax calculation

- Line 24: Credits and payments

- Line 25: Balance due/overpayment

Step 7: Prepare Required Schedules

Key schedules include:

- Schedule A: Charitable deductions

- Schedule B: Income distribution deduction

- Schedule D: Capital gains

- Schedule G: Tax computation

- Schedule K-1: Beneficiary allocations

Step 8: File the Return

- Mail to:

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0027

- E-file through approved providers

- Deadline: 15th day of 4th month after year-end

Common Mistakes to Avoid

- Missing income allocations – Must adequately report all income sources

- Incorrect distribution deductions – Complex calculations required

- Improper expense categorization – Fiduciary vs. beneficiary expenses

- Failing to reconcile with financial statements – Must match trust accounting

- Late K-1 issuance – Beneficiaries need for their filings

For complex trusts or estates, professional tax services ensure accurate reporting.

Advanced Considerations

Financial Statement Reconciliation

- Trust accounting principles

- Principal vs. income allocations

- Tax vs. book differences

- Amortization schedules

Special Trust Situations

- Grantor trust rules

- Charitable remainder trusts

- Special needs trusts

- Foreign trust reporting

State Compliance

- State fiduciary income tax

- Residency determinations

- Apportionment rules

- Local filing requirements

Final Thoughts

Proper completion of IRS Form 1041 is essential for fiduciaries to meet their tax obligations while preserving assets for beneficiaries. Executors and trustees can fulfill their duties effectively by maintaining accurate trust accounting records, reconciling with financial statements, and carefully following the latest Form 1041 instructions. For complex estates, large trusts, or special fiduciary situations, partnering with professional tax services provides the specialized expertise needed to navigate these sophisticated requirements while maximizing tax efficiency.