IRS Form 8288 serves a critical role in the U.S. tax system by facilitating the reporting and withholding of taxes when a foreign individual or entity engages in the sale of U.S. real property interests (USRPI). This form is mandated by the Internal Revenue Service (IRS) to promote compliance with tax regulations, ensuring that all transactions involving foreign sellers are properly accounted for. By requiring Form 8288, the IRS aims to safeguard the integrity of tax collection on real estate dealings that cross international borders, highlighting the importance of adherence to tax obligations in these complex transactions.

If you are a buyer or a withholding agent involved in real estate transactions, it is crucial to file Form 8288 and ensure that the correct amount of tax withholding is submitted alongside it. Neglecting this obligation can lead to significant penalties, which can complicate your financial situation. To navigate these requirements with confidence and accuracy, it may be advantageous to seek the expertise of professional tax services. Their specialized knowledge can help you manage the filing process seamlessly and avoid costly mistakes.

Table of Contents

Who Needs to File Form 8288?

- You must file Form 8288 if:

- You are a buyer of U.S. real estate from a foreign seller.

- You are a withholding agent responsible for tax withholding.

- The transaction involves a foreign person or entity selling U.S. property.

If you’re unsure whether this applies to your situation, consulting tax services can help clarify your obligations.

Step-by-Step Guide to Filling Out Form 8288

Step 1: Gather Required Information

Before filling out Form 8288, collect:

- Seller’s name, address, and Taxpayer Identification Number (TIN)

- Buyer’s details (name, address, TIN)

- Property details (address, sale price, closing date)

- Amount of tax withheld (typically 15% of the gross sale price)

Step 2: Complete Form 8288

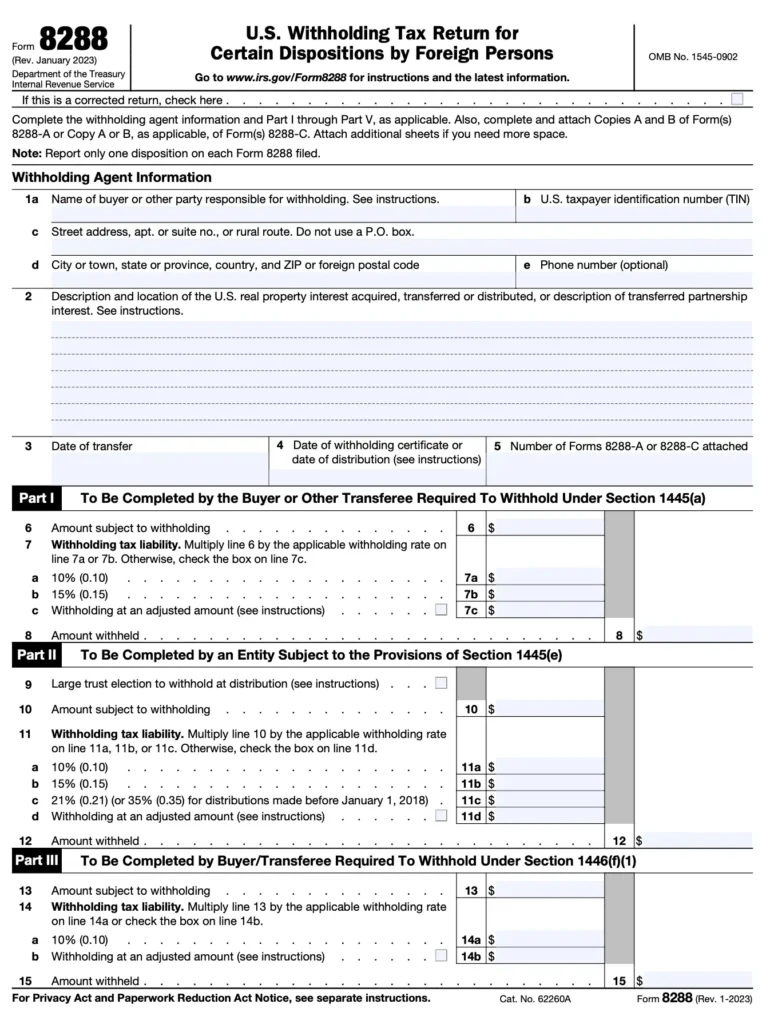

Part I – Withholding Agent’s Information

- Box 1a: Enter the withholding agent’s name (usually the buyer or closing agent).

- Box 1b: Provide the agent’s Employer Identification Number (EIN).

- Box 1c: Include the agent’s address.

Part II – Foreign Transferor (Seller) Details

- Box 2a: Seller’s name.

- Box 2b: Seller’s TIN (or “Foreign” if none).

- Box 2c: Seller’s address.

Part III – Property & Transaction Details

- Box 3a: Property address.

- Box 3b: Date of sale.

- Box 3c: Total sale price.

- Box 3d: Amount withheld (usually 15% of the sale price).

Part IV – Buyer’s Information

Step 3: Attach Form 8288-A (If Applicable)

If the foreign seller wants to apply for a reduced withholding rate, they must submit Form 8288-B before closing. Once approved, attach Form 8288-A to report the adjusted withholding amount.

Step 4: Submit Form 8288 to the IRS

- Mail the completed form to:

Internal Revenue Service

P.O. Box 409101

Ogden, UT 84409

- Deadline: File within 20 days of the property transfer date.

Step 5: Provide Copies to the Seller & IRS

- Give a copy of Form 8288 to the foreign seller for their records.

- Keep a copy for your files.

Common Mistakes to Avoid

- Missing the 20-day deadline → Late filing penalties apply.

- Incorrect withholding amount → Must withhold 15% unless reduced by IRS approval.

- Not obtaining a TIN for the seller → Can delay refunds or cause compliance issues.

For error-free filing, consider professional tax services specializing in international real estate transactions.

Final Thoughts

Filing IRS Form 8288 accurately is essential for maintaining compliance when foreign sellers engage in the transfer of U.S. real estate. By meticulously adhering to the outlined steps, you can prevent potential penalties and facilitate seamless transactions. For intricate cases that may involve unique challenges, enlisting the expertise of professional tax services can offer invaluable peace of mind and ensure precise handling of all details.