If you’re involved in a business or investment activity that resulted in a loss, the IRS doesn’t automatically let you deduct all of it—especially if you weren’t financially “at risk.” That’s where Form 6198 comes in. It calculates the portion of your loss that you’re actually allowed to claim under at-risk rules.

This guide covers everything you need to know about filing Form 6198, including when it’s required, how to fill it out line by line, and how your financial statements contribute to accurate information reporting.

Table of Contents

What Is Form 6198 and Why Is It Important?

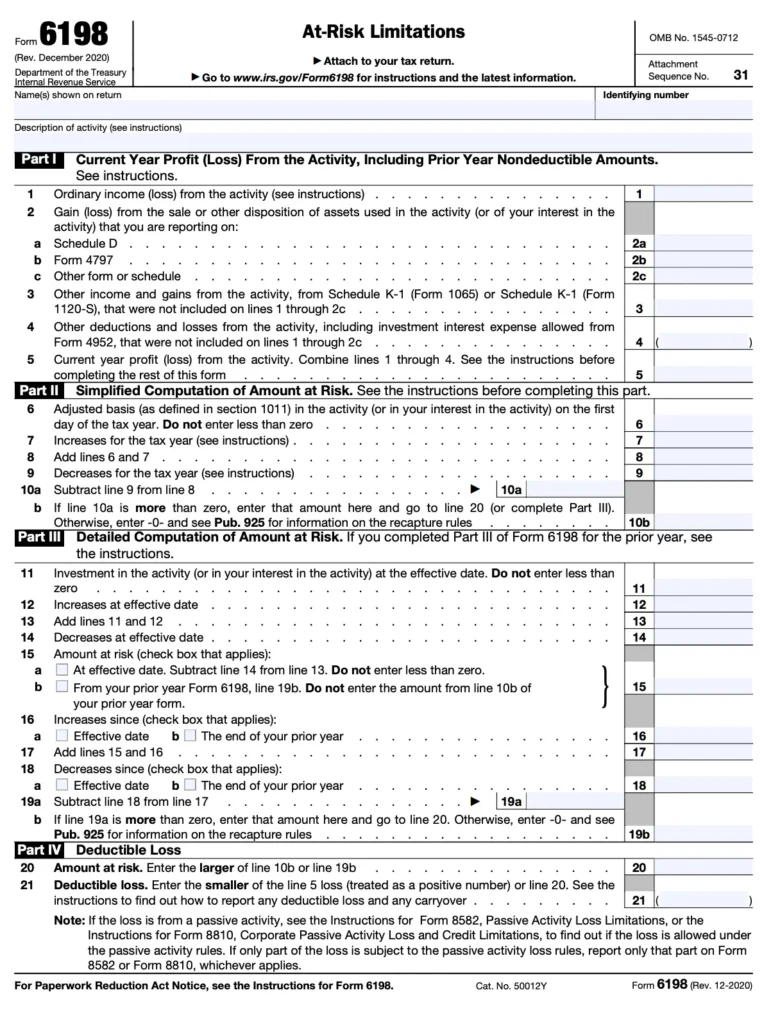

Form 6198, officially titled At-Risk Limitations, is used to figure out how much of your loss from specific business or investment activities can be deducted for the tax year. This rule ensures that you can only deduct losses up to the amount you actually had “at risk” in the venture.

You’ll typically encounter this form if you participate in:

- Partnerships or S corporations

- Real estate investments

- Farming, oil and gas, or leasing activities

It applies to activities where you aren’t personally liable for all debts—like when you use borrowed funds or nonrecourse loans.

Who Needs to File Form 6198?

You must file Form 6198 if:

- You’ve invested in a business or activity that’s subject to at-risk rules.

- The activity generated a loss for the tax year.

- You’re claiming the loss on Schedule E, C, or F, and it exceeds your at-risk basis.

You’ll file the form along with your federal income tax return (Form 1040 or Form 1040-SR).

Before You Begin: Gather the Required Information

To complete Form 6198, make sure you have:

- Your year-end financial statements

- Prior year’s at-risk amounts (if applicable)

- Records of capital contributions, loans, or adjustments during the year

- Form K-1 (if from a partnership or S corp)

- Details of any income or deductions from the activity

Being organized upfront can save you from filing errors or having to amend your return later.

When to Submit Form 6198

Form 6198 must be filed by the IRS tax deadline—usually April 15—together with your annual tax return. You cannot file this form separately.

If you’re claiming a loss from a business activity that falls under the at-risk rules, make sure to include it as a supporting form.

Step-by-Step Guide to Completing Form 6198

Now, let’s break down each section of the form and explain how to fill it out accurately.

Step 1: Start With Basic Information

At the top of the form, provide:

- Your name and Social Security Number (SSN)

- A short description of the business activity or investment you’re reporting (e.g., “Real estate rental – ABC Properties LLC”)

This helps the IRS match the form to the correct income/loss entries in your return.

Step 2: Determine the Activity Type (Part I)

Check the appropriate box to identify the activity type. Options include:

- Trade or business (Schedule C or F)

- Rental activity (Schedule E)

- Farming (Schedule F)

- Partnership or S corp (Schedule E)

If this is a passive activity, you may also need to file Form 8582 alongside Form 6198.

Step 3: Calculate Your At-Risk Investment (Lines 1–10)

Use Lines 1–10 to figure out how much money you were actually at risk for during the year. This section includes:

- Line 1: Beginning at-risk amount

- Line 2: Additional contributions or loans you’re personally liable for

- Line 3: Income from the activity

- Line 4: Deductions and distributions

- Line 10: Ending at-risk amount

These numbers should align closely with your financial statements, especially if you’re invested in multiple entities or reporting on more than one schedule.

Step 4: Report Losses and Carryforwards (Part II)

This section determines how much of the loss you can actually deduct:

- Line 11: Total loss from the activity

- Line 12: Loss allowed under at-risk rules (lesser of Line 10 or Line 11)

- Line 13: Loss disallowed and carried forward to next year

You can only deduct losses up to the amount you’re at risk for. The rest is suspended and carried forward until your at-risk basis increases.

Step 5: Recapture of Previously Allowed Deductions (Part III)

This applies if you disposed of the activity during the tax year and must recapture prior losses that were allowed but should have been disallowed due to insufficient at-risk amounts.

You’ll need to:

- Calculate total loss amounts previously deducted

- Determine if any of those losses exceeded your actual risk.

- Report the amount to be recaptured as income.

This section is complex—consider using professional tax services for help if you’re unsure.

Common Mistakes to Avoid on Form 6198

Even experienced filers make these errors:

- Using incorrect at-risk amounts from prior years

- Double-counting contributions or debt

- Not adjusting for distributions or repayments

- Forgetting to carry forward disallowed losses

To prevent issues, cross-check all entries with your year-end financial statements and partner/shareholder reports.

Final Thoughts: Don’t Overstate Your Deductions

Form 6198 keeps your deductions grounded in economic reality. If you weren’t truly “at risk” for the loss, you shouldn’t get the full tax benefit—and the IRS enforces that rule strictly.

To avoid costly mistakes, track contributions and repayments carefully using solid financial statements, and consider turning to expert tax services if your investment structure is complex.