Cash flow analysis is the process of tracking, reviewing, and interpreting the inflows and outflows of cash in your business over a specific time period. For small businesses, it is often the difference between surviving a slow quarter and closing the doors.

Key Takeaways

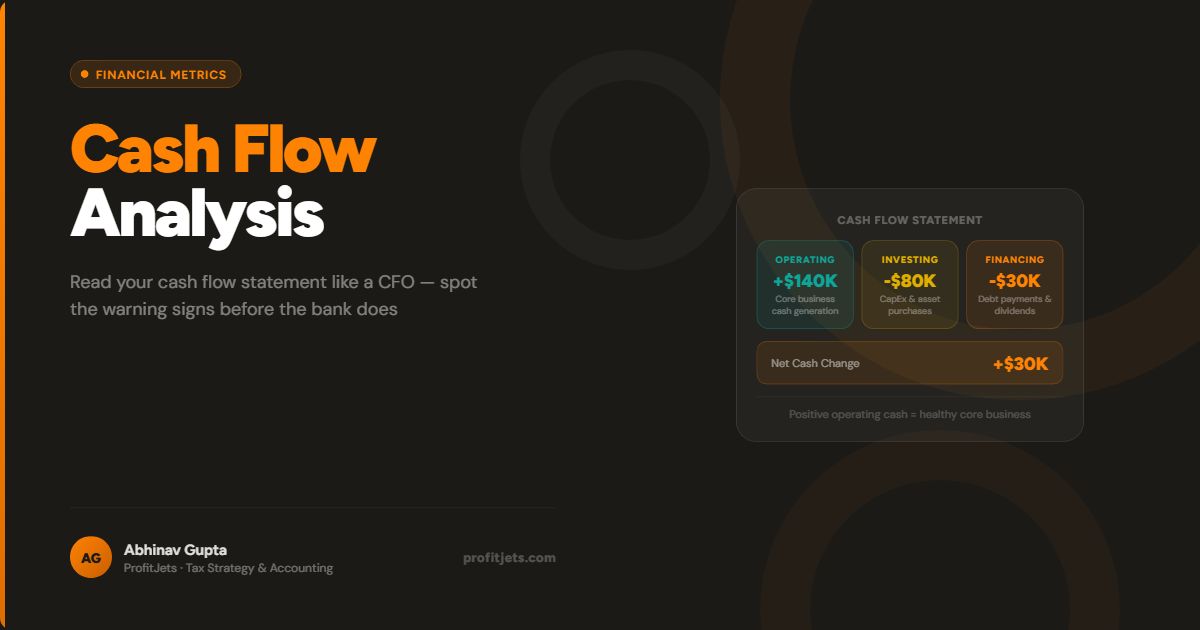

- Cash flow analysis breaks into three categories: operating, investing, and financing activities — each tells a different part of your business story.

- You can show a profit on paper while being cash-flow negative. This is especially dangerous for small businesses relying on receivables.

- Negative cash flow is not always bad — negative investing cash flow can mean you are expanding your asset base.

- Review cash flow at least monthly; weekly if your business is scaling or has seasonal patterns.

Cash flow analysis is the process of tracking, reviewing, and interpreting the inflows and outflows of cash in your business over a specific time period. It goes beyond looking at your bank balance — it organizes every dollar moving through your business into a structure that lets you see patterns, anticipate shortfalls, and make confident decisions about timing.

What Is Cash Flow Analysis?

Cash flow analysis is the process of tracking, reviewing, and interpreting the inflows and outflows of cash in your business over a specific time period. Your statement of cash flows organizes those movements into three categories:

- Operating activities — your day-to-day income and expenses: customer payments received, payroll, rent, supplier payments

- Investing activities — purchases or sales of equipment, property, and other long-term assets

- Financing activities — loans taken out or repaid, equity raised, and dividends paid

Reading all three together gives you a complete picture of where cash is coming from and where it is going.

Why Is Cash Flow Analysis Important?

Cash flow analysis gives small business owners five critical capabilities that profit reports alone cannot:

- Ensures daily operations are funded when they need to be

- Prevents cash shortages that halt operations mid-cycle

- Identifies overspending before it compounds into a crisis

- Supports budgeting and forecasting with real cash data, not just accruals

- Strengthens loan and funding applications by demonstrating financial discipline

You might show a profit on paper while being cash-flow negative — especially dangerous for small businesses that carry unpaid invoices or slow-paying customers. Profit is an accounting concept; cash is what pays the bills.

Cash Flow vs. Profit: Key Differences

| Metric | Profit | Cash Flow |

|---|---|---|

| Based on | Revenue minus expenses | Cash in minus cash out |

| Shown in | Income statement | Cash flow statement |

| Timing | May include unpaid invoices | Reflects real-time cash status |

| Focus | Long-term business success | Short-term survival and growth |

Types of Cash Flow to Track

| Type | Definition | Signal if positive |

|---|---|---|

| Operating Cash Flow (OCF) | Cash from core business operations | Business sustains itself without outside funding |

| Investing Cash Flow | Equipment purchases or asset sales | Selling assets; negative = reinvesting in growth |

| Financing Cash Flow | Loans, debt repayment, equity | New funding received |

| Free Cash Flow (FCF) | Cash after capital expenditures | Funds available for debt service or expansion |

| Levered Free Cash Flow | After interest and financial obligations | True discretionary cash remaining |

How to Conduct a Simple Cash Flow Analysis

Follow five steps to complete a basic cash flow analysis for your business:

- Gather source documents. Pull bank statements, sales invoices, payroll reports, and vendor bills for the period.

- Categorize each transaction. Sort into operating, investing, or financing activities.

- Build the statement. Use a spreadsheet or accounting software to total each category and calculate net cash flow.

- Identify patterns. Positive operating cash flow (OCF) is the most important signal — it means your core business generates cash without relying on loans or asset sales.

- Adjust strategy based on insights. Persistent negative OCF needs immediate attention; negative investing cash flow during a planned expansion is expected and healthy.

Accounting software (QuickBooks, Xero, FreshBooks) generates cash flow statements automatically from your categorized transactions. The analysis is only as good as the categorization — accurate bookkeeping is the foundation.

How to Manage Cash Flow in a Small Business

Analysis is only valuable if it drives action. Five management practices make the biggest difference for small businesses:

1. Track inflows and outflows regularly

Use accounting software or outsourced bookkeeping services to keep real-time records. Waiting until month-end to see where money went means you are always reacting rather than managing.

2. Forecast monthly and quarterly

Anticipate low-cash periods, especially if your business is seasonal. A cash flow forecast projects what your bank balance will look like 30, 60, and 90 days out so you can arrange financing before you need it, not during a crisis.

3. Monitor receivables and payables

Shorten your receivable cycle by offering early payment incentives or tightening your net terms. Pay vendor bills strategically — use the full payment window available without incurring late fees.

4. Reduce unnecessary spending

Conduct quarterly expense audits. Subscriptions, vendor contracts, and overhead tend to creep upward. A regular review catches waste before it becomes structural.

5. Build a cash reserve

Set aside a cash buffer equivalent to at least one to three months of operating expenses. This reserve absorbs seasonal dips, slow-paying clients, and unexpected costs without requiring emergency debt.

Common Mistakes in Cash Flow Management

- Relying only on profit reports. Profit does not show timing. A profitable business with slow-paying clients can run out of cash between receivables.

- Ignoring late receivables. Every dollar outstanding past 60 days is a cash flow drag. Follow up systematically.

- No forecasting during slow seasons. Seasonal businesses need to plan cash reserves during high periods to fund the lows.

- Overspending on inventory or equipment. Locking cash in assets without planning for it can leave operating accounts empty.

- Not building reserves. A single unexpected event — a major client churning, an equipment failure — can end a business that has no cash buffer.

ProfitJets provides cash flow audits and setup, ongoing monitoring through bookkeeping, tax planning with cash-based strategies, and startup financial modeling via CFO services — so your cash position is always visible and managed proactively.

Ready to get a clear picture of your cash flow and build a buffer that protects your business?

Get a Free Cash Flow AuditFrequently Asked Questions

How often should I perform cash flow analysis?

Can I do cash flow analysis without accounting software?

Is negative cash flow always bad?

How is cash flow analysis used in decision-making?

Can ProfitJets help forecast seasonal cash flow dips?

Want ongoing cash flow monitoring so you are never caught off guard?

Talk to a ProfitJets AdvisorProfitJets Editorial Team

The ProfitJets team writes practical finance guides for small and mid-sized business owners navigating growth, reporting, and strategic decisions.