You are not alone if you are approaching a tax deadline with unfinished books, delayed documents, or pending reconciliations. In most cases, for small and mid-sized businesses, tax season is rarely about disorganization, poor planning, or a lack of effort.

More often, it reflects the timing gaps in financial readiness where the deadline is approaching, invoices are still being processed, expense classifications are being finalized, and year-end reports are not fully reconciled.

However, one of the most important compliance principles often highlighted by tax advisors is this rule:

Your estimated tax liability must still be calculated and paid by the original due date.

But there is one rule about compliance that must be clear:

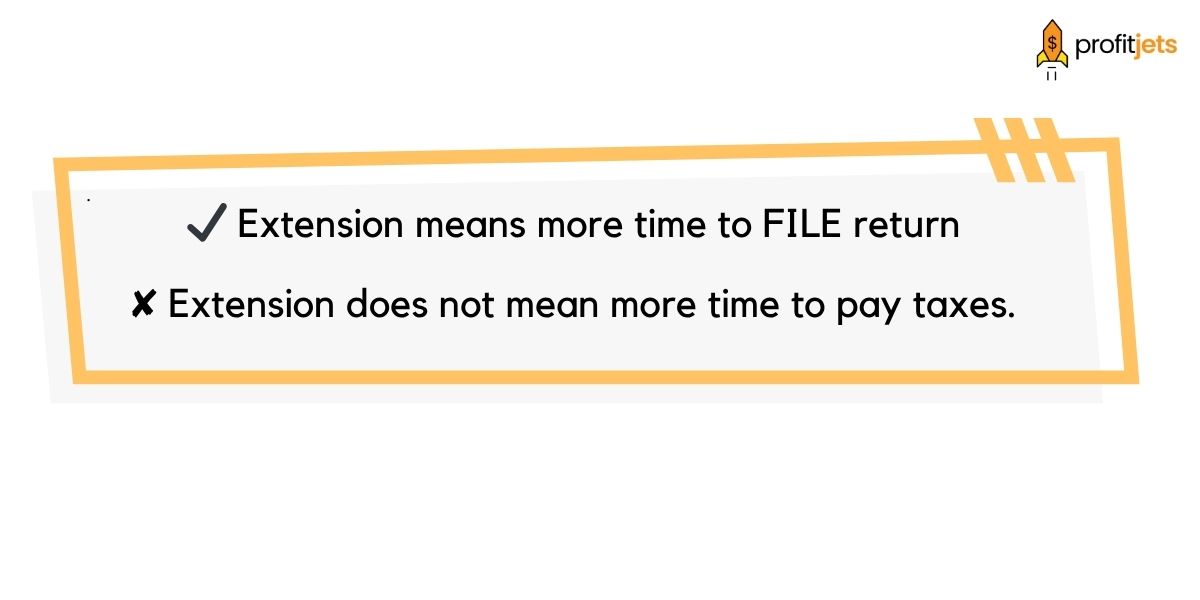

“A business tax extension must be filed on or before the original tax deadline, depending on the type of entity. It does NOT extend the time to pay taxes.”

Any estimated taxes owed must still be paid by the original due date to avoid interest and penalties.

In this guide, we’ll break down 5 easy ways to file a business tax extension online, along with key compliance rules, commonly overlooked mistakes, and a practical approach used by finance professionals to handle extensions correctly.

What Is a Business Tax Extension?

A business tax extension is a formal request submitted to the Internal Revenue Service that allows additional time to file your tax return.

Depending on the business structure, it typically provides up to six extra months to submit returns.

However, a key distinction often misunderstood is the following:

Your estimated tax liability must still be calculated and paid by the original filing deadline. Filing the extension only prevents late-filing penalties; it does not eliminate payment obligations.

In simple terms, the extension protects your filing timeline, not your payment obligation.

Once this is clearly understood, the extension process becomes less about delay and more about structured financial preparation.

Reasons Why Businesses File Tax Extensions

Contrary to common perception, tax extensions are not a sign of poor planning. In many environments, businesses use tax extensions as a risk management tool when financial data is still being processed, and it takes time to review the details.

Based on observing patterns, businesses typically file extensions due to the following reasons:

- Pending tax documents such as K-1s or 1099s,

- Unreconciled bank or ledger accounts,

- Complex or multi-stream revenue structures,

- Multi-state or multi-entity reporting requirements, and

- Additional internal review needed before final submission.

In these cases, rushing the filing process can lead to avoidable issues such as misreported income, missed deductions, or inconsistencies that may require future amendments.

A properly filed extension allows businesses to move from provisional figures to verified financial statements, which significantly improves reporting accuracy.

Easy Ways to File a Business Tax Extension Online

Today, businesses have multiple reliable methods depending on their financial complexity. Filing an extension is now much easier because of the digital transformation in tax compliance.

These are the five most common and useful methods:

1. IRS e-File System

The most direct and official method is filing through the IRS electronic filing system.

This method is widely used because it offers several advantages:

- Submits your extension directly to the IRS database

- Provides immediate confirmation of acceptance

- Reduces manual filing errors

- Ensures faster processing compared to paper filing

However, professionals often caution that accuracy in tax estimation remains critical even when using official systems.

2. Tax Filing Software Platforms

Many businesses rely on tax software solutions to streamline the extension process.

These platforms typically:

- Guide users through structured filing steps

- Auto-select relevant IRS forms

- Assist in estimating tax liability based on financial data

- Reduce manual calculation and entry errors

This method is widely adopted by small and mid-sized businesses that prefer guided automation without fully outsourcing tax filing.

3. Through a Tax Professional or CPA

For businesses with more complex financial structures, working with a CPA or tax advisor is often the most reliable approach.

Experienced tax professionals use:

- File extensions on behalf of the business

- Perform accurate tax liability estimation

- Identify compliance risks early in the process

- Align filing with broader tax planning strategies

Who is it relevant for? This approach is especially relevant for businesses with:

- Multi-entity operations,

- Cross-border transactions, and

- High-volume or diverse revenue streams

While it involves additional cost, it significantly reduces compliance risk and improves accuracy in both filing and estimation.

4. Accounting Platforms with Built-In Features

The ability to file taxes, including submitting extensions, is becoming more and more common in modern accounting software.

This approach is effective because it:

- Uses real-time financial data from bookkeeping systems,

- Maintains consistency between accounting and filing records,

- Reduces manual data transfer and reconciliation errors, and

- Improves accuracy in tax estimation.

For businesses already using cloud accounting systems, this becomes a natural extension of their financial workflow rather than a separate process.

5. Authorized IRS e-File Providers

Another reliable option is using IRS-authorized third-party e-file providers.

These providers are specifically approved to handle compliant submissions and typically offer the following:

- Secure and encrypted filing systems

- Built-in validation checks for error reduction

- Faster processing times

- Submission tracking and confirmation logs

This method is commonly used by businesses looking for a balance between automation, compliance assurance, and cost efficiency, without fully outsourcing to a CPA.

Key Steps you Should Not Overlook while Filing a Business Tax Extension

Regardless of how you choose to file your extension, the underlying compliance steps remain the same. These are not just steps to follow; they have a direct effect on whether your extension is valid and whether you avoid penalties.

In practice, businesses should ensure the following:

Step 1: Identify Your Tax Deadline (For 2025 tax year)

→ Based on your entity type

Step 2: Select the Correct IRS Form

→ Choose based on your business structure

- Form 7004 for Corporations, Partnerships, LLCs

- Form 4868 for Sole Proprietors

- Form 8868 for exempt organizations

Step 3: Estimate Your Tax Liability

→ Use current financial data, prior-year returns, and revenue trends

Step 4: Pay Estimated Taxes Due

→ Ensure payment is made before the original deadline

Step 5: Retain Filing Confirmation

→ Save IRS acknowledgment for records, compliance, and audit proof

Why Accurate Tax Estimation Matters (With reference to the IRS)

One of the most commonly misunderstood aspects of filing a tax extension is the role of tax estimation.

Penalties can arise from both late filing and underpayment. However, businesses that file their extensions on time typically avoid late-filing penalties but may still face penalties for underpayment of taxes.

As outlined by the Internal Revenue Service, penalties are often imposed not because the extension was filed late but because the tax paid was lower than the actual liability.

In practical terms:

- Late filing penalties can go up to 5% per month

- Late payment penalties typically add 0.5% per month

- Interest continues to accrue until the balance is fully paid

Filing a valid extension helps avoid late-filing penalties only if the return is submitted within the extended deadline.

Practical Insight

In many cases, penalties are not triggered because the extension was filed late, but because the tax paid was lower than the actual liability.

Businesses that treat this step seriously tend to

- Avoid unnecessary penalties

- Reduce last-minute adjustments

- Maintain better financial clarity going into the final filing.

What Happens After You File an Extension?

Once your extension is successfully filed and accepted by the IRS, you receive additional months to complete and submit your return.

However, from a financial management perspective, the value of this period depends entirely on how it is used. Well-structured businesses treat this phase as a financial review window, not an extension of delay.

During this time, finance teams typically:

- Fully reconcile accounts and ledgers,

- Correct bookkeeping discrepancies,

- Review expense and income classifications,

- Identify missed deductions or credits, and

- Validate financial statements before final submission.

External accountants or advisors are also engaged during this phase to ensure final accuracy.

The objective is not just to meet the extended deadline but to improve the quality and reliability of the final return.

Benefits of Filing a Business Tax Extension

When used strategically, a tax extension offers measurable advantages beyond additional time.

1. Improved Accuracy

Reduced deadline pressure leads to more complete and reliable reporting.

2. Lower Compliance Risk

Accurate filings reduce the likelihood of audits, amendments, or corrections.

3. Better Financial Clarity

Businesses gain a more accurate understanding of their financial position before filing.

4. Stronger Tax Planning

Additional time allows for better evaluation of deductions, credits, and liabilities.

How Profitjets Helps Businesses Manage This Better

Profitjets supports businesses by:

- Managing accurate and timely extension filings,

- Providing structured tax estimation support,

- Maintaining clean and audit-ready bookkeeping systems,

- Ensuring compliance across reporting cycles,

- Strengthening long-term financial clarity and reporting accuracy.

With Profitjets, your tax extension is part of a structured, error-free compliance process that helps your business grow over time.

FAQs: Frequently Asked Questions

1. Does filing a tax extension reduce my tax liability?

No, filing a tax extension does not reduce your tax liability. It only gives you additional time to file your return. Your total tax obligation remains the same and must be estimated and paid by the original deadline to avoid penalties and interest.

2. Can I avoid penalties if I file an extension on time?

Filing an extension helps you avoid late-filing penalties, but it does not protect you from late payment penalties or interest. If your estimated tax payment is insufficient, penalties may still apply even when the extension is correctly filed.

3. What happens if I underestimate my taxes while filing an extension?

Underestimating taxes is one of the most common compliance risks. Even with a valid extension, the IRS may impose late payment penalties and interest on the unpaid portion. This is why many businesses take a conservative approach to estimation.

4. Is filing a tax extension a red flag for the IRS?

No, filing an extension is a standard and widely accepted practice. Many well-managed businesses use extensions strategically to ensure accuracy and completeness.

5. Can I still file my return before the extended deadline?

Yes. An extension provides up to six additional months, but you can file your return at any time within that period. In fact, many businesses file earlier once their financials are fully reconciled and verified.

6. Do all business entities follow the same extension process?

No, the extension process varies based on the entity type.

For example:

- Corporations, partnerships, and LLCs typically use Form 7004

- Sole proprietors use Form 4868

- Exempt organizations use Form 8868