IRS Form 1094-C serves as the transmittal form for employers filing under the Affordable Care Act’s Employer Shared Responsibility Provisions. This critical document must accompany all 1095-C forms when reporting:

- Employee health coverage offers

- Plan affordability details

- Employer size determinations

- Transition relief eligibility

Table of Contents

Who Must File Form 1094-C?

You’re required to complete this form if your business is:

- An Applicable Large Employer (ALE) with 50+ full-time employees

- Part of a controlled or affiliated service group

- Claiming any transition relief provisions

- Self-insured and meeting ALE thresholds

Important: Even if you qualify for exemptions, you may still need to file. Professional tax services can assess your specific requirements.

Step-by-Step Guide to Completing Form 1094-C

Step 1: Determine Your ALE Status

Calculate your workforce size using:

- Full-time employees (30+ hours/week)

- Full-time equivalent employees (FTEs)

- Monthly measurement method data

Note: Seasonal worker exceptions may apply – consult Form 1094-C instructions carefully.

Step 2: Gather Required Documentation

Prepare:

- Employee census data

- Health plan enrollment records

- Financial statements showing premium costs

- Prior year filings for reference

- Corporate structure documents (for aggregated groups)

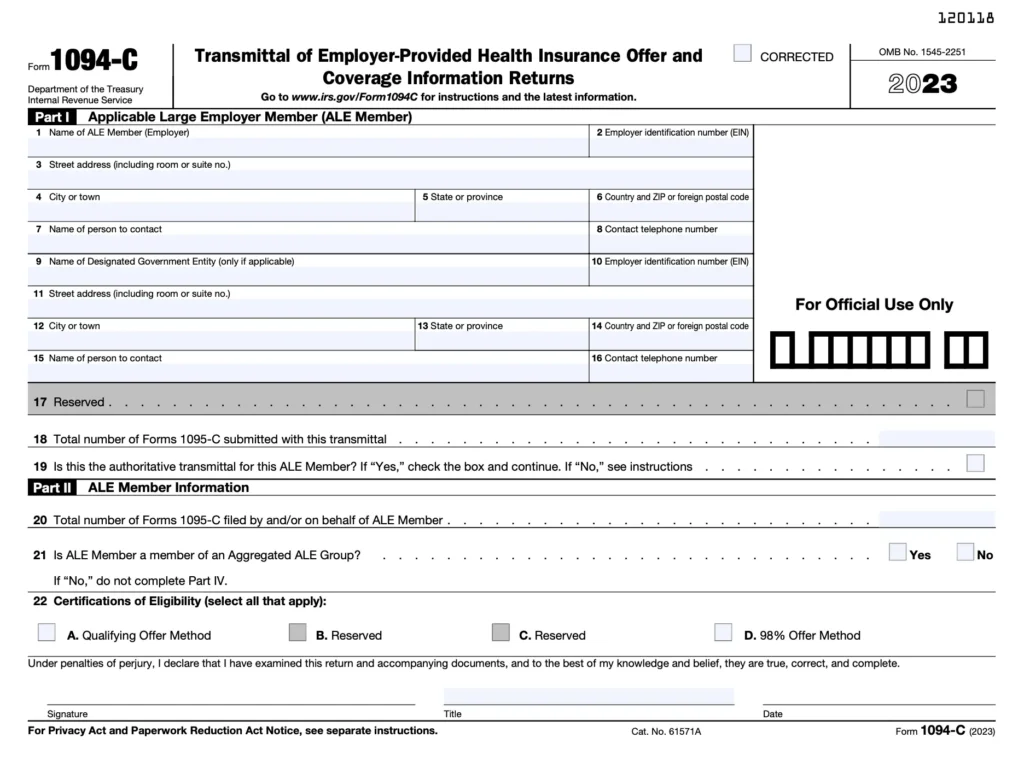

Step 3: Complete Part I – Employer Information

- Boxes A-D: Legal business name, EIN, address, and contact

- Box E: Total number of 1095-C forms submitted

- Box F: Certifications of eligibility for transition relief

Step 4: Complete Part II – ALE Member Information

For each ALE member:

- Line 16: Member name and EIN

- Line 17: Full-time employee count

- Line 18: Total employee count

- Line 19: Offer of coverage codes

- Line 20: Plan start month

Step 5: Complete Part III – ALE Details

- Line 21: Certify minimum essential coverage offered

- Line 22: Qualifying offer method used (if applicable)

- Line 23: Section 4980H transition relief

- Line 24: Aggregated group indicator

Step 6: Complete Part IV – Authoritative Transmittal

Designate one Form 1094-C as authoritative for:

- Aggregated ALE groups

- Multiple EIN filings

- Consolidated reporting

Step 7: Submit to the IRS

- File electronically through the ACA Information Returns system

- Deadline: February 28 (paper) or March 31 (electronic)

- Keep copies with supporting financial statements for 4 years

Common Mistakes to Avoid

- Incorrect employee counts – Misclassifying FTEs triggers penalties

- Missing transition relief codes – Available for specific plan years

- Mismatched 1095-C totals – Must reconcile with transmittal

- Late filings – Penalties up to $290 per form

- Incomplete corporate structure reporting – Critical for controlled groups

For complex organizational structures, professional tax services ensure accurate reporting.

Advanced Reporting Considerations

Financial Statement Reconciliation

- Align premium costs with payroll records

- Verify affordability percentages (9.12% for 2023)

- Document safe harbor elections

Correcting Errors

- Use Form 1094-C/1095-C corrections process

- Different procedures for in-year vs. prior-year amendments

- Statute of limitations considerations

State Reporting Requirements

- Many states now mandate duplicate ACA filings

- Varying deadlines and formats

- Potential additional disclosures

Final Thoughts

Proper completion of IRS Form 1094-C is fundamental to ACA compliance for applicable large employers. By methodically gathering employee data, maintaining supporting financial statements, and carefully following the latest Form 1094-C instructions, organizations can meet their reporting obligations while minimizing penalty risks. For businesses with complex structures, frequent workforce changes, or those implementing new health plans, partnering with professional tax services provides invaluable assurance and expertise in navigating these intricate requirements.