You pull up your balance sheet because you need an answer, not a vocabulary lesson. Can you cover the next 30 to 90 days, and will the bank be comfortable, or are any of these numbers setting you up for a cash crunch?

- Unreconciled accounts can show phantom cash and hide real liabilities: verify the data before you read a single ratio.

- Read the balance sheet as a cash timing map. What turns into cash soon vs. what demands cash soon is the question that matters.

- Misclassified current vs. non-current items create a liquidity mirage: the balance sheet says fine, the bank account says otherwise.

- The current ratio and quick ratio lie when current assets are not truly cash-like. Always check A/R aging and inventory quality first.

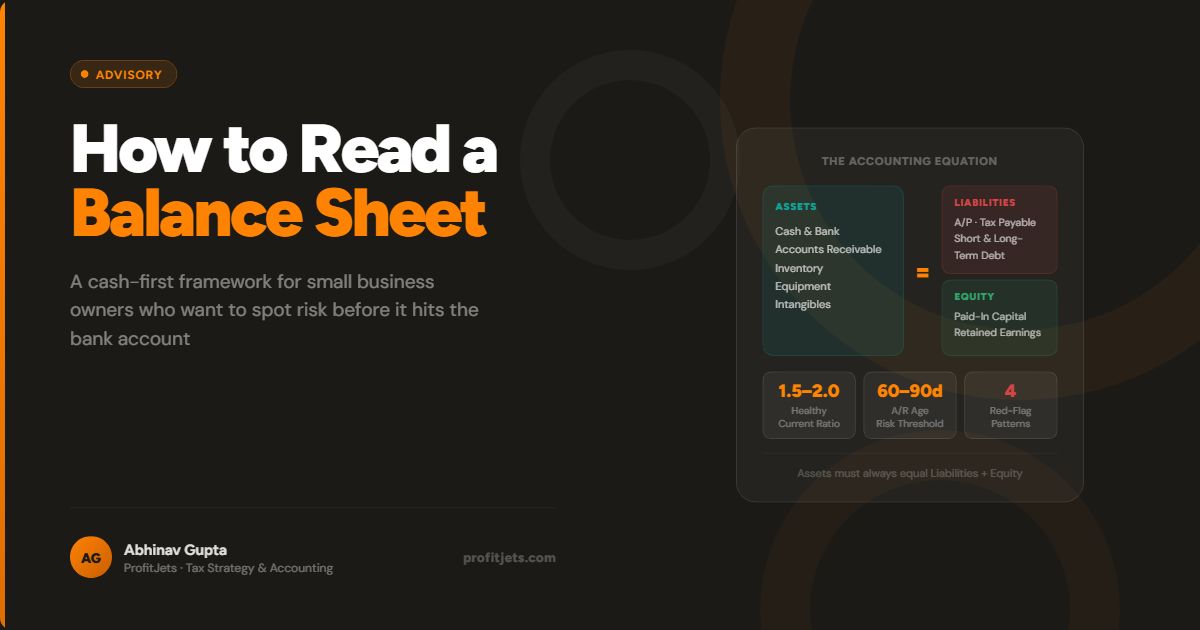

- Four red-flag patterns predict most cash surprises: rising A/R with flat cash, growing inventory without sales, expanding tax liabilities, and loan balances that barely move.

This guide shows you how to read a balance sheet like an operator. You’ll start by checking whether the statement is even trustworthy, because unreconciled accounts and bad classifications can make good ratios meaningless. Then you’ll read it as a map of near-term cash pressure: what can turn into cash soon and what will demand cash soon. By the end, you’ll know what to look for in assets and liabilities, which two liquidity ratios to run first, and what specific questions to ask your bookkeeper or CFO advisor when something doesn’t add up.

Common Healthy Current Ratio

A/R Age That Signals Risk

Questions to Ask Monthly

Start with: Is This Balance Sheet Trustworthy?

Before you analyze anything, make sure it ties out. If it isn’t, you’ll waste time debating whether your current ratio is good when the real issue is that unreconciled accounts or misclassifications are distorting both the balance sheet and the P&L. Case in point: an unreconciled credit card can leave expenses sitting in limbo and inflate cash, right up until a payment clears and your numbers swing for no operational reason.

If your cash and credit cards aren’t reconciled, the balance sheet can show phantom cash and hide real liabilities until payments clear. Every ratio you run on top of that is built on noise.

| Trust Check Item | What to Confirm | Why It Matters |

|---|---|---|

| Bank & credit cards | Reconciled through the statement date; no old unreconciled items | Prevents phantom cash and understated liabilities/expenses |

| A/R & A/P aging | Past-due A/R is collectible; A/P includes real bills with no duplicates or missing invoices | Avoids overstated assets or understated payables |

| Loans | Balances tied to lender statements; current portion of long-term debt classified as current | Keeps liquidity view and debt timing accurate |

| Payroll & sales tax payable | Tied to the latest filings and payment confirmations | Reduces compliance risk and hidden near-term cash drains |

| Payment processors (Stripe/Shopify) | Identify clearing accounts and confirm they’re reconciled | Prevents phantom cash from unsettled deposits |

Read It Like a Cash Map

Treat the balance sheet like a cash map, not a vanity scorecard. Anyone selling health from one page is kidding themselves, and QuickBooks Online won’t save you from timing. Look first at what can turn into cash soon (cash and receivables) versus what will demand cash soon (vendor bills and the next 12 months of loan principal). The balance sheet vs. income statement distinction matters here.

Profit can look strong while cash gets tight when A/R drifts to 60–90 days, and rent and payroll still hit every two weeks. If you start reading it this way, you’ll stop asking “Is equity positive?” and start asking “What’s going to pull cash out of my account before cash comes in?”

The Cash Map Mindset

Accounts receivable that consistently collects late can force you to fund payroll and vendors before customer cash hits the bank. The balance sheet shows the gap; the cash map shows when it hurts.

Current vs. Non-Current: The Classification Trap

You renew your line of credit, feeling covered, then a sudden shortfall hits because next quarter’s payments were sitting in the wrong place on the statement. The damage isn’t the debt; it’s the timing you didn’t see coming.

If current and non-current are wrong, your liquidity read is a mirage. You can look like you have a safe buffer (high current ratio) simply because long-term debt payments got left out of current liabilities, or because old receivables and stale inventory got parked in current assets even though they won’t turn into cash soon. That’s how owners get blindsided: the balance sheet says fine, but the bank account says otherwise.

When something feels off, don’t debate the ratio. Ask what’s sitting in the wrong bucket: Is the next 12 months of loan principal included in current liabilities? Are any A/R balances effectively uncollectible but still labeled current? If this month’s classification choices aren’t consistent with last month’s, your trend line is noise, not insight.

Assets: What’s Real and Usable?

A founder once pointed to a six-figure current asset balance and still had to delay payroll, because half of it couldn’t turn into spendable cash in time. On paper, it looked safe; in the bank account, it wasn’t.

Don’t treat current assets as money you can spend. If you do, you’re basically trusting Xero to do your thinking. You can look asset-rich on paper and still come up short on cash when those assets don’t convert on your timeline, or ever.

Start by pressure-testing what’s actually usable. Cash should tie to reconciled bank accounts, not wishful undeposited funds or payment processor balances that take days to settle. A/R should be judged by collectability and timing: if a big chunk sits 60–90+ days past due, it’s not funding next payroll even if it’s labeled current. Inventory only helps liquidity if it’s sellable at something close to its recorded value; slow-moving, seasonal, or obsolete stock can make your current ratio look strong while you can’t pay bills.

Prepaids are a common trap: they’re real, but they don’t pay vendors. If you prepaid six months of insurance and software, your assets rise, but you didn’t create a runway; you just moved cash into future coverage. Ask your bookkeeper to flag which current assets convert to cash in 30 days versus eventually.

Liabilities: What Must Be Paid Next?

Read liabilities as your cash payment schedule, not a moral verdict. The surprises usually aren’t the obvious vendor bills; they’re timing items that don’t come with a weekly invoice but still hit your bank account fast, like payroll tax payable building up each pay run or the current portion of a term loan sitting below the fold.

To surface hidden drains, scan for four lines that commonly explain “Why is cash tight?” even when sales look fine: A/P that’s past due (you’re borrowing from vendors, until you can’t), payroll and sales tax payable (you’re holding money that isn’t yours), current maturities of long-term debt (principal due in the next 12 months), and deferred revenue (cash received, but you still owe delivery and the costs that come with it). If you only treat liabilities as “bills we haven’t paid yet,” you’ll miss the obligations that can force decisions before you feel them operationally.

These are held in trust for the government and must be remitted on a strict schedule. A balance that grows month over month means the business is funding operations with money it doesn’t own. The IRS and state tax authorities don’t negotiate on remittance timelines.

Equity and Retained Earnings: What Story Is It Telling?

Equity is the net worth left after liabilities, and retained earnings (sometimes shown as an accumulated deficit when negative) is the running total of profits you’ve kept in the business minus losses and owner distributions. If you hand-wave this, you are playing with fire. A negative number usually means the business has racked up losses over time, not that this month went badly, and it can also show up in a growth phase before profitability.

Don’t wave it off as just accounting, though. If retained earnings keep falling while you’re taking distributions, you’re shrinking your cushion against a slow quarter and making lenders more nervous. Ask your accountant to reconcile: how much of the change came from net income versus owner draws/dividends versus a capital contribution.

The Two Ratios That Matter First (and When They Lie)

A lot of small-business guidance pegs an ideal current ratio around 1.5–2.0, but the number only matters in the context of how fast your cash converts and how fast your bills come due. The same ratio can mean breathing room in one business and next week’s scramble in another.

Start with liquidity. This is your dashboard warning light for the next 30–90 days.

Current Ratio

Gives a first-pass buffer. Many SMB guides cite ~1.5–2.0 as a common healthy range, but the only useful target fits your industry and cash cycle.

Quick Ratio (Acid Test)

Removes inventory optimism. More conservative and often more honest as a near-term liquidity indicator than the current ratio alone.

These ratios lie when current assets aren’t really cash-like: inventory that won’t sell at book value, or A/R that collects in 60–90 days while payroll is due now. If the ratios look fine but cash is still tight, ask for an A/R aging-by-due-date and an inventory obsolescence review instead of chasing another ratio.

Want a CFO reading this alongside you every month?

ProfitJets fractional CFO advisors review your financials monthly and flag what the numbers mean for your specific situation.

Red-Flag Patterns Owners Should Recognize

One team kept celebrating record months until their payables stack forced an emergency vendor call, and a tax payment got pushed to the edge. The balance sheet had been warning them for weeks if anyone had read the pattern instead of the totals.

Some balance sheets don’t look bad. They look unlikely. And if you ignore that, you are asking for a cash surprise, even if Bill.com is humming. When you spot these recurring patterns, stop interpreting and start verifying: the operational consequence is usually a cash surprise or a compliance problem.

-

01

A/R climbing while cash stays flat

Collections are slipping or revenue is being booked faster than cash comes in. The gap between these two lines predicts a cash shortfall before it shows up in the bank.

-

02

Inventory rising without a matching sales lift

Slow-moving or overstated stock is propping up current assets. The current ratio looks strong; the cash position doesn’t match it.

-

03

Payroll/sales tax payable growing month after month

You’re funding operations with money you’ll have to remit. This is one of the fastest ways to trigger IRS enforcement action while the income statement still looks fine.

-

04

Loan balances that barely change

Payments may be getting miscoded, or the current portion isn’t being tracked. Either way, it can blindside your next 12 months’ cash plan when the balloon comes due.

What to Ask Your Bookkeeper or CFO Advisor

You don’t need more ratios; you need answers that change what shows up on next month’s balance sheet. This is the get-the-books-in-order checklist, not a debate club. If you accept unexplained swings or vague labels (like “Other current assets”), you’re choosing to manage the business on noise.

-

1

What balances are reconciled to third-party statements as of this date, and what isn’t?

Bank accounts, credit cards, loans: every major line should tie to a statement. If it doesn’t, start there.

-

2

What’s in A/R over 60–90 days, what’s the collection plan, and what should be written off?

You want names, amounts, and a realistic assessment. A total balance without aging detail is not useful.

-

3

What inventory or other current assets are unlikely to convert to cash in 30 days?

This stress-tests your current ratio in real terms. If the answer is “I’m not sure,” the ratio may be misleading you.

-

4

What did you reclassify between current and non-current this month, and why?

Reclassifications should be documented and explained. Any shift that moves a liability from long-term to current is especially important to flag.

-

5

Which liabilities will hit cash in the next 2–4 weeks?

Taxes, loan principal, vendor pileup: this question converts the balance sheet into a short-term cash planning tool. Combined with question two, it gives you a rolling liquidity view.

“You don’t need more ratios; you need answers that change what shows up on next month’s balance sheet.”Abhinav Gupta, ProfitJets

Frequently Asked Questions

Why Does My Balance Sheet Show Negative Equity?

Negative equity means liabilities exceed assets on paper, often because you’ve accumulated losses over time (retained earnings are negative) or you’ve taken distributions faster than profits built equity. It can also happen in a growth phase before profitability. Your next step is to ask what’s driving it: cumulative losses, owner draws, or balance sheet errors like missing assets or overstated liabilities.

What Are “Due to Owner” or “Due From Owner” Lines, and Should I Worry?

These lines track money moving between you and the business that isn’t categorized as payroll or distributions, like paying a vendor on a personal card or reimbursing yourself irregularly. If the balance keeps growing or flips directions often, ask for a clear explanation and documentation, because lenders and tax preparers will treat sloppy owner-loan activity as a risk, and it can mask real expenses.

What Is Deferred Revenue, and Why Is It a Liability If I Already Got Paid?

Deferred revenue is cash you collected before you delivered the product or service, so it represents an obligation to perform or refund. If it’s rising, pressure-test whether you have the capacity and costs covered to fulfill what you owe, not just whether your bank balance looks higher.

Why Doesn’t Profit Match the Cash in My Bank Account?

Profit reflects accrual timing and non-cash items, with A/R and A/P usually doing most of the damage. If cash is falling while profit looks fine, ask which working-capital line moved the most (A/R, inventory, A/P, taxes payable) and whether collections are slower than the bills coming due.

Is Negative Retained Earnings the Same as “We Had a Bad Month”?

No. Retained earnings are cumulative: the net total of profits and losses over the life of the business, minus distributions. If it’s getting worse while revenue is up, ask whether you’re actually losing money, taking heavy draws, or carrying balance sheet items (like stale A/R) that should be written off.

How Often Should a Small Business Owner Review the Balance Sheet?

Monthly is the standard. A balance sheet reviewed only at tax time is a compliance document. A balance sheet reviewed every month, alongside the income statement and cash flow statement, gives you enough lead time to act on trends (climbing A/R, growing tax liabilities, shifting debt classifications) before they become emergencies.

Make the Balance Sheet a Monthly Operating Habit

When you start reading the balance sheet as a cash map instead of a scorecard, you stop looking for a verdict and start looking for timing problems. Reconcile first, read assets by how fast they convert, read liabilities by when they’re due, and ask the five questions every month. That practice is what turns a standard financial report into an early-warning system for the things that actually threaten the business.

Get a CFO Reading Your Balance Sheet Every Month

ProfitJets advisors review your financials monthly, flag risks before they become problems, and give you the clarity to make faster decisions.

See How It WorksAbhinav leads the advisory team at ProfitJets, working with founders and small business owners on financial reporting, tax planning, and outsourced CFO services. He specializes in helping businesses translate their financials into operational clarity.