<!doctype html>

Operating income and EBITDA both measure profitability, but they answer different questions. Choosing the wrong metric for a business decision can lead to the wrong conclusion. Here is exactly when to use each one.

Key Takeaways

- Operating income shows profit from core business operations after all operating expenses, excluding interest and taxes.

- EBITDA adds back depreciation and amortization on top of operating income, giving a broader view of cash-generative ability.

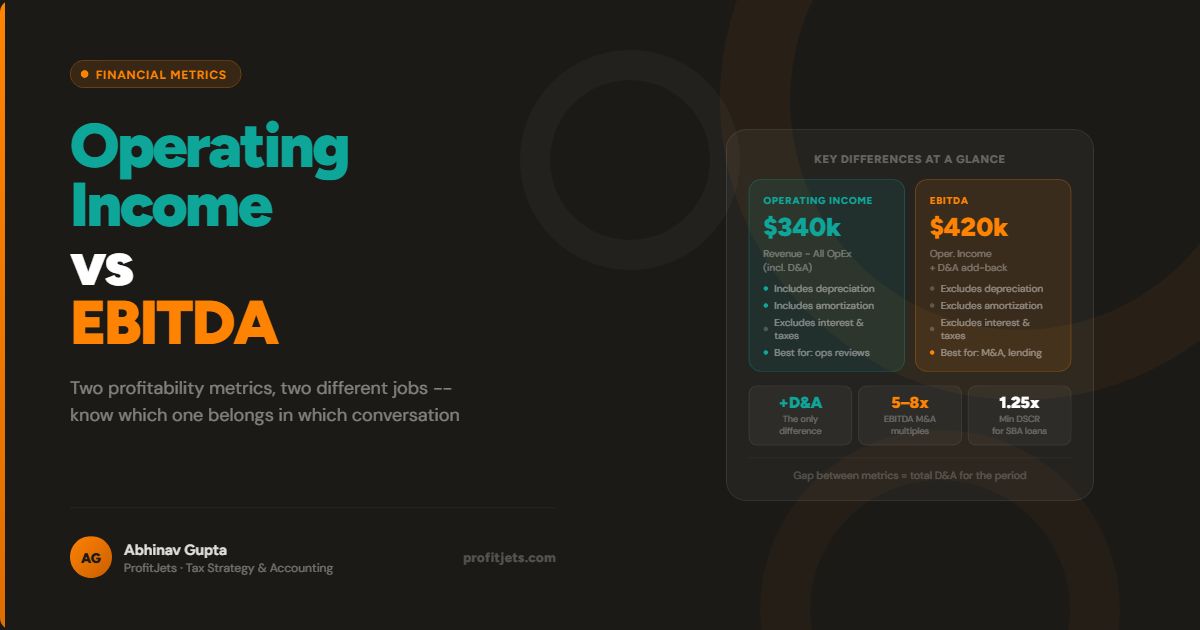

- Operating income is best for period-to-period performance comparisons within the same company. EBITDA is better for cross-company valuation.

- Yes, operating income can be negative while EBITDA is positive, when high depreciation and amortization expenses dominate the difference.

- EBITDA should always be used alongside other metrics since it excludes working capital changes, capex, and taxes.

What Is Operating Income?

Operating income (or operating profit) shows a company’s profit from core business operations. It is calculated by subtracting operating expenses from revenue. It excludes non-operating activities like interest and taxes, revealing operational efficiency without the influence of external financial factors.

This makes operating income particularly useful for understanding how well the actual business runs, independent of how it is financed or how it is taxed.

Operating income includes depreciation and amortization, unlike EBITDA. This means it reflects the real cost of asset use over time, making it a more conservative profitability measure than EBITDA for capital-intensive businesses.

How to Calculate Operating Income

Formula: Operating Income = Revenue – Operating Expenses

Operating expenses include cost of goods sold, salaries, rent, utilities, depreciation, and amortization. They exclude interest expense and income taxes.

Revenue of $500,000 minus $300,000 in operating expenses = $200,000 operating income. Interest paid on a business loan would not reduce this figure; it is handled below the operating income line.

Advantages of Using Operating Income

- Shows the business’s ability to profit from its main activities, independent of financing decisions

- Allows evaluation of operational efficiency period over period

- Provides a standardized measure that is comparable across companies within the same industry

What Is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It excludes non-operating costs and non-cash expenses, providing a broader profitability perspective. Investors and analysts use it in valuations and financial analysis to assess the cash flow a business generates before accounting decisions (like depreciation schedules) and financing choices (like debt structure) distort the picture.

How to Calculate EBITDA

Formula: EBITDA = Operating Income + Depreciation + Amortization

$200,000 operating income + $30,000 depreciation + $20,000 amortization = $250,000 EBITDA. The business generates $50,000 more in EBITDA than operating income because those non-cash charges are added back.

Advantages of Using EBITDA

- Gives a clearer view of cash-generative ability by excluding non-cash expenses like depreciation and amortization

- Effective valuation tool for comparing businesses across industries with different capital structures

- Focuses on operational performance independent of financial and accounting decisions

Operating Income vs EBITDA: Key Differences

| Dimension | Operating Income | EBITDA |

|---|---|---|

| Scope | Core operations only | Broader profitability view |

| Non-Cash Items | Includes D&A as a cost | Excludes D&A; better for cash flow proxy |

| Cross-Company Use | Best within same company over time | Eliminates interest and tax differences across capital structures |

| Valuation | Less commonly used in M&A multiples | Standard denominator in EV/EBITDA valuation multiples |

| Limitation | Affected by D&A policy choices | Ignores working capital changes, capex, and taxes |

When to Use Operating Income vs EBITDA

Use operating income when you want to assess operational efficiency and compare performance period over period within the same company. It is the cleaner measure of how well the business executes its core model over time, because it holds depreciation policy constant.

Use EBITDA when investors or analysts are evaluating cash flow, particularly when comparing companies with different tax rates, depreciation schedules, or capital structures. EBITDA is the standard metric in acquisition pricing, lender underwriting, and cross-industry benchmarking.

EBITDA is considered effective but should always be used with other metrics. It does not account for working capital changes, capital expenditures, or taxes. A business with strong EBITDA but heavy capex requirements or growing working capital needs may have far less actual cash than the EBITDA number suggests.

Not sure which metric matters most for your business or lender conversations?

Talk to a CFO AdvisorFrequently Asked Questions

What is the main difference between operating income and EBITDA?

What is the main difference between operating income and net income?

Is EBITDA a good measure of profitability?

Can operating income be negative while EBITDA is positive?

When should a small business owner focus on EBITDA?

Need help preparing EBITDA and operating income reporting for investors or lenders?

Schedule a Free ConsultationProfitJets Advisory Team

The ProfitJets team helps small and mid-sized business owners understand financial metrics and use them to make smarter operating decisions.