While businesses focus on growth and scaling, it’s equally important to understand how dividend reporting and tax liabilities can impact your overall financial outcomes.

As per Internal Revenue Service (IRS) regulations, Schedule C is an attachment to Form 1120 that must be filed along with Form 1120 for the corporate income tax return.

This allows corporations to report dividend income and claim eligible special deductions, making it a key component in accurate tax computation and compliance.

Why Schedule C of Form 1120 Matters for C Corporations

When you own a C corporation, tax compliance means going beyond the numbers on your income statement. You need to think strategically about how your income is structured and what deductions you’re eligible to use.

Schedule C plays a direct role in this by helping C corporations to:

- Report the dividend income received,

- Calculate eligible deductions such as the Dividends Received Deduction (DRD), and

- Reduce the overall taxable income in line with IRS regulations.

In simple terms, Schedule C acts as a bridge between dividend income and tax optimization. Without it, corporations cannot claim key deductions that directly reduce tax liability.

It is important to understand the following:

- Schedule C is required only if dividend income or special deductions exist

- That said, these decisions directly impact your bottom-line tax liability.

- Any error in Schedule C can affect taxable income and total tax liability

Who Must File Schedule C of Form 1120?

Schedule C is required for:

- C corporations reporting dividend income.

- Corporations claiming DRD or other special deductions.

- Certain foreign corporations filing U.S. tax returns.

If there are no dividends or applicable deductions, Schedule C may not be required. However, as businesses grow and invest across entities, the need for Schedule C becomes more common.

The Dividends Received Deduction (DRD): What You Need to Know

What it is and who gets it: The DRD is a tax break available to C corporations that receive dividend income from other companies. Individuals don’t qualify, as this is strictly for corporations filing Form 1120. The deduction lets you reduce your taxable income by the dividends you receive.

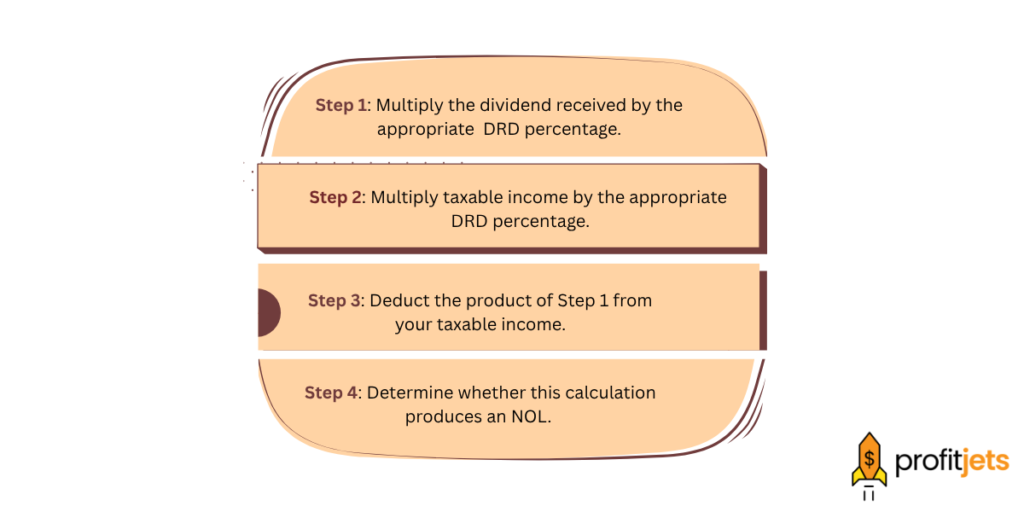

Step-by-Step DRD Calculation of Form 1120

- DRD: Dividends Received Deduction

- NOL: Net Operating Loss

Note:

If an NOL is created or increased, the product of Step 1 is your DRD.

If no NOL is created, the deduction is limited to the lesser of Step 1 or Step 2.

The problem it solves: Your Corporate income can get taxed multiple times as it moves through different hands.

Picture this: A subsidiary earns money and pays corporate tax on it (first tax). Then it sends dividends to the parent company, which pays tax again on those dividends (second tax).

If the parent corporation then pays those dividends out to its shareholders, that imposes a third round of taxes. This triple-taxation problem is expensive and inefficient.

The DRD eases this burden by allowing the parent corporation to deduct the dividends it receives, reducing the second layer of tax.

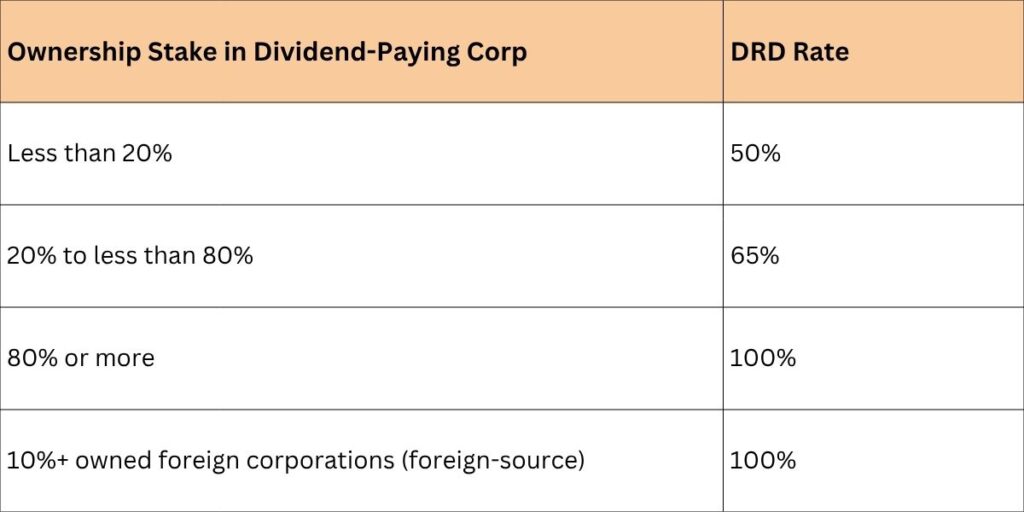

How much you can deduct: The amount of the deduction depends on how much of the dividend-paying company you own. Higher ownership means a larger deduction rate.

Where to claim it: You report the DRD on Schedule C when you file Form 1120.

DRD Rates Based on Ownership

The deduction percentage depends on the corporation’s ownership stake in the dividend-paying entity:

For example, if Corporation X receives $10,000 from Corporation Y and owns less than 20%, it can deduct $5,000 (50%). If it owns 40% of Corporation Y, the deduction rises to $6,500 (65%). If it owns 80% or more, it may deduct the full $10,000 (100%).

- <20% ownership → $5,000 deductible

- 40% ownership → $6,500 deductible

- ≥80% ownership → Full $10,000 deductible

Important timing rule: To qualify for the DRD, you need to own the stock for at least 46 days during a 90-day window. This window starts 45 days before the stock’s ex-dividend date. The IRS has this rule to prevent improper usage.

Taxable Income Limitation on DRD

While the DRD offers significant tax savings, it is not always fully available. In most cases, the deduction is subject to a taxable income limitation.

This means the DRD cannot exceed a certain percentage of the corporation’s taxable income.

However, there are two important exceptions:

- If the corporation qualifies for a 100% DRD, the limitation does not apply

- If applying the DRD results in a Net Operating Loss (NOL), the full deduction can still be claimed

Because of this, accurate calculation becomes critical. Even small errors in applying these limits can directly impact the final tax liability.

What Does Not Qualify for DRD

All dividends are not eligible for the deduction. Understanding exclusions is just as important as understanding eligibility.

Common non-qualifying dividends include:

- Dividends that are received from the Real Estate Investment Trusts (REITs).

- Dividends from the tax-exempt organizations.

- Shares that do not meet the holding period requirements.

- Dividends from the debt-financed stock.

Incorrect classification of these items can lead to disallowed deductions and compliance issues. This is one of the most common areas where corporations make filing mistakes.

Special Deductions Beyond DRD

Schedule C of Form 1120 is not limited to dividend-related deductions. It also supports additional deductions that influence overall tax outcomes.

1. Net Operating Loss (NOL)

- Can offset up to 80% of taxable income

- Carried forward indefinitely

- Must follow FIFO (first-in, first-out) utilization

2. Section 250 Deduction

- Applies to corporations with international operations

- Covers GILTI (Global Intangible Low-Taxed Income) and FDII (Foreign-Derived Intangible Income).

- Helps reduce taxable income on foreign earnings

These deductions are especially relevant for growing businesses with multi-entity or cross-border structures.

Where things go wrong

Even small slip-ups like ownership percentages that don’t match your records, math errors, or numbers that don’t tie together can impose an IRS rejection or land you in an audit.

Things often go wrong if,

- You’re misidentifying who owns what percentage of the company.

- You’re missing the holding period requirement (45 days in a 90-day window for DRD eligibility).

- You’re applying the wrong DRD percentage based on your ownership stake.

- You don’t have receipts, documents, or records to back up what you’re claiming.

The IRS catches these inconsistencies because they’re looking for them. That’s why precision and documentation aren’t optional; they’re the difference between a clean filing and a problem.

Expert Takeaway

Most businesses treat Schedule C as a compliance requirement. But it’s actually a tool that impacts three critical areas:

- Getting deductions right. Missing deductions costs you money. Claiming the wrong ones invites audit risk. You need to know which ones actually apply to your business.

- Avoiding filing mistakes. One misplaced number can trigger penalties, interest, and IRS scrutiny. Precision matters here.

- Matching your tax approach to your growth. If your business is scaling, your tax strategy should reflect that. Schedule C is where that strategy gets documented.

The reality is this: a missed deduction or careless error on Schedule C can expose you to thousands in additional tax liability.

The difference between a routine filing and one that actually protects your interests comes down to how carefully you approach it.

Why Businesses Choose Profitjets for Corporate Taxes

Filing Schedule C correctly takes more than just knowing the rules; you need to understand how your business fits into the bigger tax picture.

Our team of tax professionals at Profitjets helps handle the parts that save you money:

- Set up your tax structure correctly.

- File Schedule C accurately and on time

- Find deductions you’d miss on your own.

- Keep you compliant with IRS rules.

The Impact: Lower risk of costly mistakes, more confident filings, and a tax approach that actually supports where your business is heading.

Frequently Asked Questions (FAQs)

Q1. What is Schedule C (Form 1120), and why is it required?

Schedule C (Form 1120) is used by C corporations to report dividend income and claim deductions like the DRD. It plays an important part in reducing taxable income, as it directly impacts the corporation’s final tax liability and IRS compliance.

Q2. Who needs to file Schedule C with Form 1120?

Any C corporation that receives dividend income or claims special deductions such as DRD or NOL must file Schedule C. As businesses grow and invest across entities; filing this schedule becomes increasingly common.

Q3. Are Dividends Received Deduction (DRD) rates the same every year?

The DRD rates are widely set at 50%, 65%, or 100% based on ownership thresholds under current tax law. While these rates have remained consistent since the Tax Cuts and Jobs Act, corporations must review IRS updates annually for any regulatory changes.

Q4. What records are required to support Schedule C (Form 1120) filings?

Corporations should maintain documentation such as stock ownership records, dividend statements, and financial schedules to support DRD claims.

Q5. What are common mistakes when filing Schedule C (Form 1120)?

Frequent mistakes include incorrect DRD calculations, failing holding period rules, misclassifying dividends, and missing documentation. These errors can lead to disallowed deductions, higher tax liability, or IRS audits.