You might view it as another step in a routine process, but Form 1120 is the official record of your corporation’s financial position, capturing income, deductions, and credits reported to the federal government. It is the legal document through which your corporation accounts for every dollar of income, every deductible expense, and every tax credit.

For many C corporations, every tax year becomes a hassle, often leading to unnecessary penalties. A missed schedule, misclassified deduction, or incorrect reconciliation often imposes an IRS review that costs far more than the error itself.

This guide equips you with the clarity and precision needed to handle Form 1120 for the 2025 tax year, filed in 2026.

What Is Form 1120 and Why Does It Exist?

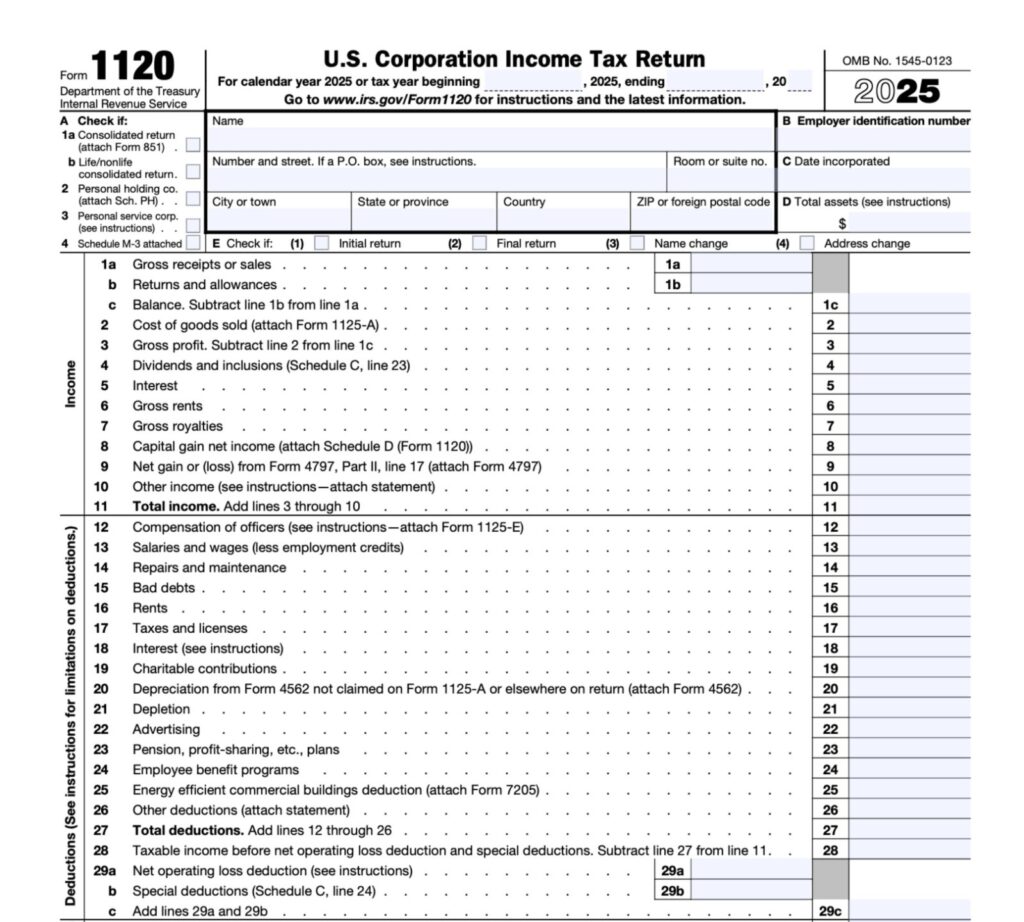

Form 1120, or U.S. Corporation Income Tax Return, is the Internal Revenue Service (IRS) form that domestic C corporations use to report their annual income, gains, losses, deductions, credits, and final tax liability. It is the foundational tax document for any corporation taxed as a C corp under Subchapter C of the Internal Revenue Code.

One detail that surprises many newly formed corporations is that filing is mandatory regardless of whether the business generated taxable income during the year. The IRS requires all domestic corporations, including those in bankruptcy and those with zero revenue, to file Form 1120 annually.

The concept is that the IRS uses this return not just to collect taxes but to gain a complete view of a corporation’s financial position. It also helps track ownership structure and monitor the ongoing compliance status of every C corporation operating in the United States.

Who Must File Form 1120?

The following entities are required to file Form 1120 each year:

Entities Required to File:

- All domestic C corporations, including those operating at a loss or with no income, should file form 1120.

- Newly incorporated or inactive corporations must still file form 1120.

- Corporations that have dissolved, which must file by the 15th day of the 4th month after the date of dissolution (final return required).

- Domestic entities including LLCs and partnerships that have elected to be classified as a C corporation by filing Form 8832, Entity Classification Election.

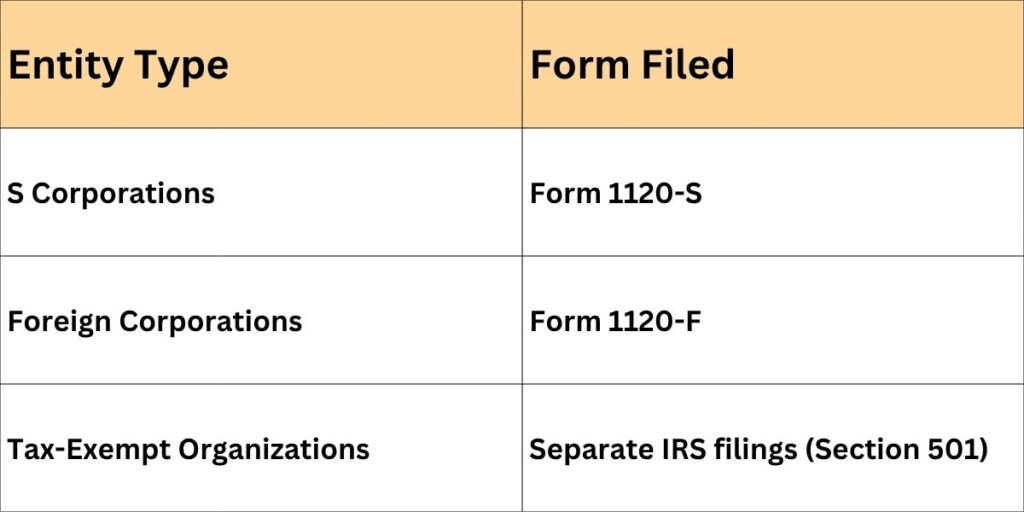

Entities That Do NOT File Form 1120:

Entities classified as S corporations file Form 1120-S instead, foreign corporations use Form 1120-F, and tax-exempt organizations under Section 501 are generally exempt from the Form 1120 requirement.

Understanding these distinctions is essential when advising on entity structure or handling a corporate reorganization.

The C Corporation Tax Structure You Must Understand First

Before completing Form 1120, it is essential to understand how C corporations are taxed. Unlike pass-through entities, C corporations are taxed at the entity level, creating a structure that directly affects reporting and planning decisions.

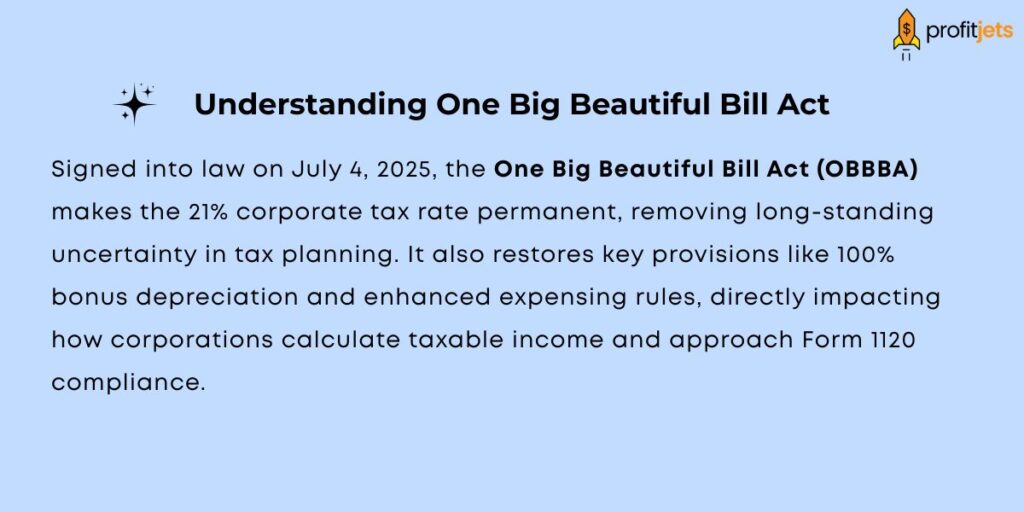

The C corporations are subject to a flat 21% federal income tax rate on all taxable income. Introduced under the Tax Cuts and Jobs Act and made permanent by the One Big Beautiful Bill (OBBBA), this rate applies uniformly regardless of income level. As a result, tax strategy shifts away from bracket management and toward optimizing deductions and timing.

Defining Double Taxation

A defining feature of this structure is double taxation. Corporate profits are taxed once at the entity level and again when distributed as dividends to shareholders. These distributions are not deductible at the corporate level, and shareholders cannot offset corporate losses on their personal returns.

Qualified Business Income (QBI) deduction

Another important consideration is that C corporations are not eligible for the Qualified Business Income (QBI) deduction. This benefit is reserved for pass-through entities such as S corporations, partnerships, and sole proprietorships, and the OBBBA made that 20% QBI deduction permanent.

This makes entity-selection decisions even more vital for growing businesses weighing C-corp status.

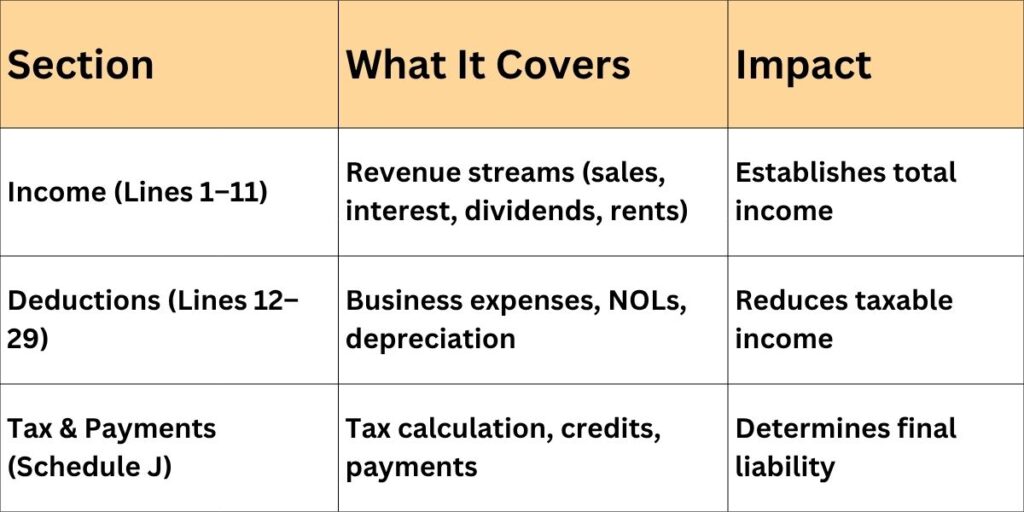

Key Sections of Form 1120 at a Glance

Form 1120 is organized into three primary sections, each building on the last to arrive at the corporation’s final tax liability.

Key Schedules of Form 1120: When They Apply and Why They Matter

Understanding when a schedule is required and what it reveals to the IRS is where experienced preparers distinguish themselves from generalist filers.

- Schedule A is required for corporations with cost of goods sold. It reports opening inventory, purchases, labor costs, and closing inventory, arriving at the gross profit figure that feeds into the income section.

- Schedule C covers dividends and special deductions, including the dividends-received deduction (DRD), a provision that allows corporations to deduct a portion of dividends received from other domestic corporations, reducing the effective tax burden on intercorporate investment income.

- Schedule G is imposed when any entity, individual, or estate owns directly 20% or more or indirectly 50% or more of the corporation’s total voting power. It maps the ownership structure for IRS review.

- Schedule L is the balance sheet per the books. It must reconcile with the financial statements and is required for most corporations. An exemption applies only to corporations with total receipts under $250,000 and total assets under $250,000.

- Schedule M-1 reconciles book net income to taxable income. Common differences include depreciation timing under MACRS versus GAAP, meals and entertainment limitations, Section 174 R&D amortization adjustments, and the treatment of tax-exempt interest.

- Schedule M-3 replaces Schedule M-1 for corporations with total assets of $10 million or more. It requires significantly more granular disclosure of book-to-tax differences and is a primary audit-risk indicator the IRS monitors closely.

Variants of Form 1120: Are You Filing the Right One?

Filing the wrong variant of Form 1120 is a compliance error that requires an amended return and, in some cases, imposes penalties.

The most common variants and their filing contexts are listed as follows:

- Form 1120-S: For S corporations that have elected pass-through tax status. Income and losses flow to individual shareholder returns via Schedule K-1.

- Form 1120-F: For foreign corporations doing business in the United States or deriving U.S.-source income.

- Form 1120-H: For qualifying homeowner associations that meet the 60% gross income test for membership dues and assessments.

- Form 1120-W: A worksheet used to calculate and submit quarterly estimated tax payments throughout the year, not an annual return.

- Form 1120-C: For corporations operating on a cooperative basis, including agricultural and horticultural cooperatives governed by unique patronage income rules.

What C Corporations Should Watch For (2026)

Regulatory changes continue to reshape the Form 1120 compliance landscape, making it essential for finance leaders to stay ahead of new developments.

The most significant update is the permanent 21% corporate tax rate. While this removes uncertainty from long-term planning, it also eliminates any strategic advantage of delaying income in anticipation of rate changes.

Corporations filing 10 or more total returns annually must now e-file Form 1120 under IRS regulations. Larger corporations may also be subject to the Corporate Alternative Minimum Tax (CAMT), which applies a 15% minimum tax on adjusted financial statement income.

The 1099-NEC and 1099-MISC reporting threshold will increase from $600 to $2,000 beginning with payments made in calendar year 2026.

For the 2025 tax year (filed in 2026), the existing $600 threshold still applies. Corporations should update vendor payment tracking systems ahead of the 2026 transition.

Deadlines and Penalties Every C Corp Must Know

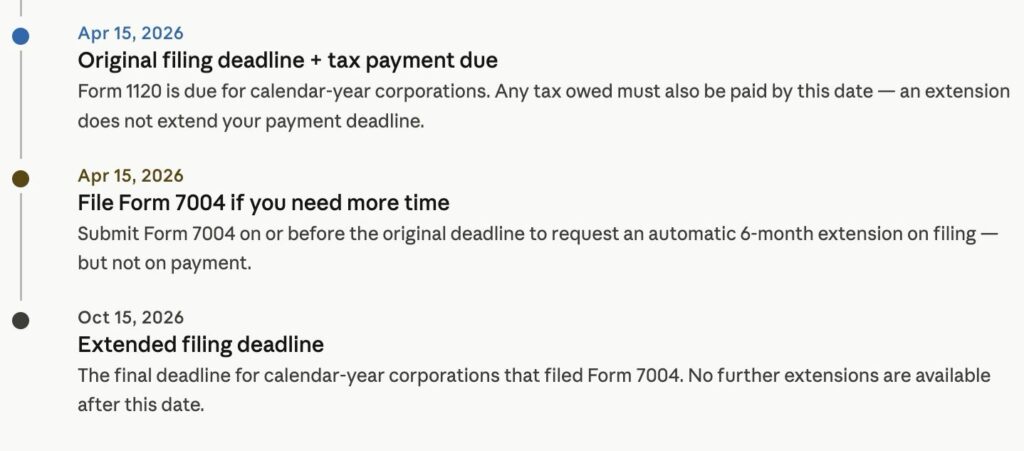

Form 1120 deadlines are fixed and directly tied to your corporation’s tax year. For calendar-year corporations, the return for the 2025 tax year is due on April 15, 2026.

Filing Timeline for quick reference

For C corporations that need additional time to prepare their return, the IRS allows up to a 6-month extension by filing Form 7004 on or before the original due date. This extends the Form 1120 filing deadline to October 15, 2026, for calendar-year (Jan 1 to Dec 31) corporations.

However, please note that an extension only applies to filing the return, not paying taxes.

Any estimated corporate tax liability needs to be paid by April 15, 2026, to avoid late payment penalties and interest charges.

Making sure your C corporation tax return is filed correctly and on time gives you enough time to review it instead of rushing to meet deadlines.

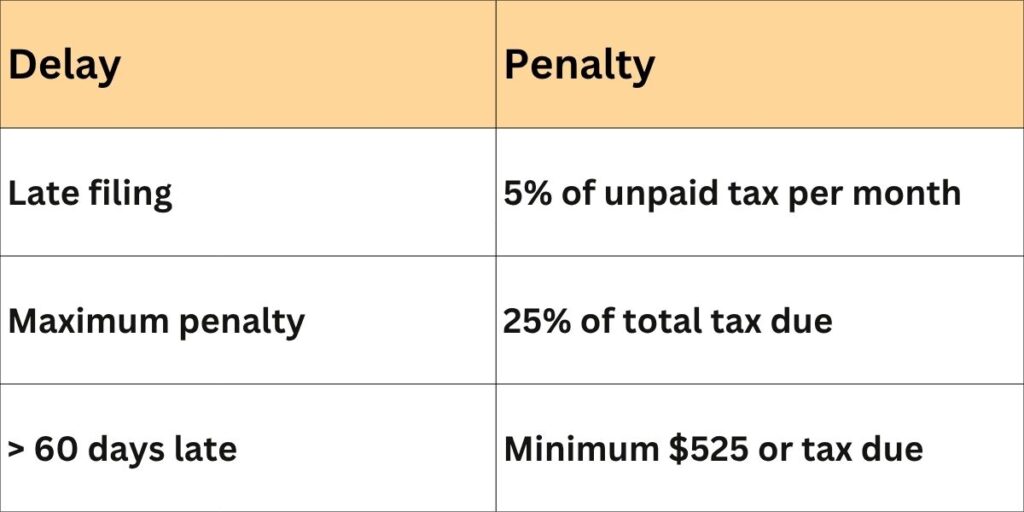

Penalty Structure

Failure to file on time can quickly become expensive. For example, a corporation with a $100,000 tax liability that delays filing by five months could face $25,000 in penalties, excluding interest.

Filing an extension on time is one of the simplest ways to avoid this exposure

Staying aligned with these deadlines is essential to maintaining compliance and avoiding unnecessary financial risk.

How Profitjets Ensures Accuracy with C corporation filing

Our team of experts at Profitjets helps C corporations streamline their entire tax process from preparation and review to final filing. Our team ensures your financials are aligned, your deductions are optimized, and your return is filed accurately and on time.

Frequently Asked Questions (FAQs)

Q1. Can a corporation file Form 1120 with no income?

Yes, C corporations must file Form 1120 even if they have no income or business activity during the year. Filing is mandatory to maintain compliance with IRS regulations and avoid penalties.

Q2. What is the difference between Form 1120 and Form 1120-S?

Form 1120 is used by C corporations, which are taxed at the entity level. Form 1120-S is used by S corporations, where income and losses pass through to shareholders and are reported on individual tax returns.

Q3. Do C corporations need to make estimated tax payments?

Yes, C corporations are required to make quarterly estimated tax payments if they expect to owe $500 or more in taxes. These payments help avoid underpayment penalties and ensure compliance throughout the year.

Q4. Should small businesses outsource Form 1120 preparation?

Small and mid-sized businesses often outsource Form 1120 preparation to reduce errors, ensure compliance, and save time. Professional support helps navigate complex tax rules and optimize deductions effectively.

Q5. How do you calculate taxable income on Form 1120?

Taxable income on Form 1120 is calculated by subtracting allowable business deductions, depreciation, and net operating losses from total corporate income. Accurate classification of income and expenses is essential to ensure compliance and avoid IRS adjustments.