Financial ratios condense vast financial statements into digestible numbers. By comparing different elements of your financial statements, they reveal crucial aspects of your business health: profitability, efficiency, liquidity, and solvency. Here are the ones that matter most for small businesses.

Key Takeaways

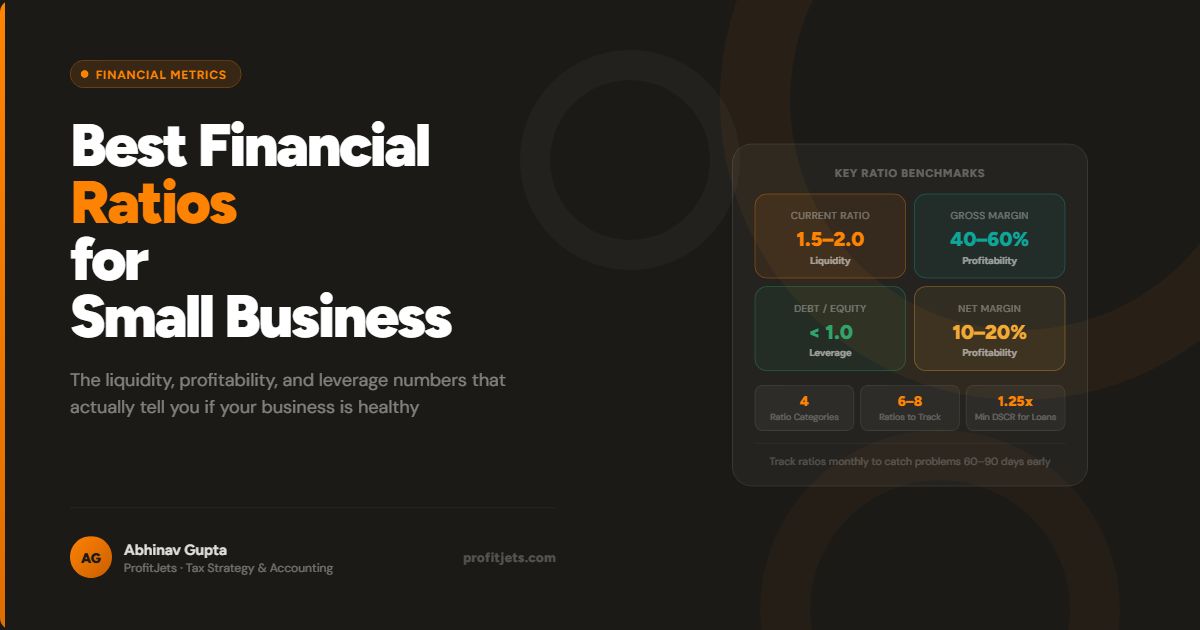

- A current ratio between 1.5 and 2 is generally considered healthy for small businesses, indicating sufficient assets to cover liabilities.

- Ratios are only useful when compared to industry benchmarks and tracked over time – a single snapshot is not enough context.

- Liquidity ratios tell you if you can pay short-term bills. Profitability ratios tell you if the business model works. You need both.

- Investors and lenders analyze financial ratios to assess creditworthiness and potential for success. Know yours before they ask.

- Review key financial ratios at least quarterly to stay informed about performance and make timely adjustments.

What Is a Financial Ratio?

Think of financial ratios as performance metrics that condense vast financial statements into digestible numbers. By comparing different financial statement elements, ratios reveal crucial aspects of your business health: profitability, efficiency, and solvency.

Think of it this way: you would not judge a book by its cover, but glancing at its page count gives you a rough idea of its length. Similarly, financial ratios offer quick glimpses into your business’s financial story. The real value comes not from any single ratio in isolation, but from tracking them over time and comparing them to industry benchmarks.

What Is the Importance of Financial Ratios for Small Businesses?

For small businesses, navigating the financial landscape can be challenging. Financial ratios provide invaluable tools to:

- Assess your financial health: Identify strengths and weaknesses to make intelligent decisions about allocating resources, investments, and growth strategies.

- Benchmark against industry standards: Compare your ratios to competitors or industry averages to gauge your relative performance.

- Track progress over time: Monitor your ratios over months or years to identify trends, measure the effectiveness of financial decisions, and celebrate improvements.

- Secure funding: Investors and lenders often analyze financial ratios to assess your business’s creditworthiness and potential for success.

- Communicate financial health: Present clear and concise financial data using ratios to stakeholders, investors, and potential partners.

Liquidity Ratios

Liquidity ratios measure your ability to meet short-term obligations. These are the first ratios to check when cash feels tight.

Current Ratio

Formula: Current Assets / Current Liabilities

Measures your capability to meet short-term obligations (within a year). A ratio of 2:1 is generally considered healthy, meaning you have twice as many current assets as current liabilities. Below 1.0 means you technically cannot cover near-term bills from current assets alone.

Quick Ratio (Acid Test)

Formula: (Current Assets – Inventory) / Current Liabilities

A stricter measure of short-term liquidity that excludes less-liquid inventory. Aim for a quick ratio above 1. If your current ratio looks healthy but your quick ratio does not, check your inventory quality and A/R aging before assuming you have adequate liquidity.

A current ratio of 1.2 might be fine for a service business with fast-collecting receivables and minimal inventory, but tight for a retailer with slow-moving stock. Always compare against your specific industry benchmarks, not generic rules of thumb.

Profitability Ratios

Profitability ratios reveal whether your business model is actually generating returns, and how much margin you retain at each level of the income statement.

Gross Profit Margin

Formula: (Revenue – Cost of Goods Sold) / Revenue x 100%

Indicates the percentage of revenue remaining after accounting for direct production costs. Industry benchmarks are crucial for comparison here – a 40% gross margin is excellent in one sector and thin in another.

Net Profit Margin

Formula: Net Income / Revenue x 100%

Reveals the percentage of revenue remaining after accounting for all expenses. A higher margin indicates better overall profitability. If your gross margin is strong but net margin is thin, the problem is in your overhead and operating expenses.

Enhance your net profit margin by increasing revenue, reducing costs, optimizing pricing strategies, and improving operational efficiency. Start with the gross margin line – if unit economics are broken, operating efficiency alone cannot save the overall margin.

Solvency Ratios

Solvency ratios measure your reliance on debt and your ability to meet long-term obligations. These matter most when you are seeking loans, attracting investors, or planning major capital expenditures.

Debt-to-Equity Ratio

Formula: Total Liabilities / Total Equity

Measures your reliance on debt financing compared to owner investment. A lower ratio indicates more robust financial stability. A high ratio means creditors bear more of the risk than owners do, which makes lenders and investors nervous.

Debt-to-Asset Ratio

Formula: Total Liabilities / Total Assets

Expresses the proportion of assets financed by debt. Industry benchmarks provide context – capital-intensive businesses naturally carry higher ratios than service businesses. A ratio above 1.0 means liabilities exceed assets, which signals insolvency risk.

Efficiency Ratios

Efficiency ratios measure how effectively you manage your assets to generate revenue. They are especially useful for spotting operational drag before it hits the income statement.

Inventory Turnover Ratio

Formula: Cost of Goods Sold / Average Inventory

Measures how efficiently you manage inventory. A higher ratio indicates faster inventory turnover and potentially reduced carrying costs. A falling turnover ratio means stock is sitting longer, tying up cash and risking obsolescence.

Accounts Receivable Turnover Ratio

Formula: Net Credit Sales / Average Accounts Receivable

Indicates how quickly you collect customer payments. A higher ratio suggests efficient collection practices. Convert this to days outstanding (365 / turnover ratio) to see your average collection period in plain terms.

Need help calculating and interpreting these ratios for your business?

Talk to a CFO AdvisorAdditional Ratios Worth Knowing

Return on Investment (ROI)

Formula: Net Income / Investment

Measures the return generated on a specific investment. Useful for evaluating individual projects, equipment purchases, or marketing spend. Always specify what “investment” means in your calculation to keep comparisons valid.

Earnings per Share (EPS)

Formula: Net Income / Number of Outstanding Shares

Indicates profitability per share of stock. Relevant for publicly traded companies or businesses with multiple equity holders who want to understand per-share value creation.

How to Use Financial Ratios

Financial ratios are valuable tools but should not be interpreted in isolation. Consider these factors:

| Factor | What to Do | Why It Matters |

|---|---|---|

| Industry benchmarks | Compare your ratios to relevant industry averages | A ratio that looks weak in one sector can be strong in another |

| Trends over time | Track ratios over several periods to identify direction | A declining ratio is more alarming than a low but stable one |

| Full financial context | Analyze complete financial statements alongside ratios | Ratios are snapshots; statements show the full picture |

| Professional guidance | Consult a certified bookkeeper or accountant for interpretation | Ratios can mislead without knowledge of accounting quality |

Frequently Asked Questions

Why are financial ratios important for small businesses?

How often should I review these financial ratios?

Can I calculate these ratios manually?

What is a good current ratio for a small business?

How can I improve my net profit margin?

Want a monthly financial ratio dashboard built for your business?

Schedule a Free ConsultationProfitJets Advisory Team

The ProfitJets team helps small business owners understand, track, and act on the financial metrics that drive sustainable growth.