IRS Form 940 (Employer’s Annual Federal Unemployment Tax Return) is used to report and pay unemployment taxes owed under the Federal Unemployment Tax Act (FUTA). This tax funds state workforce agencies and provides unemployment benefits to workers who lose their jobs.

Table of Contents

Who Must File Form 940?

You must file if you:

- Paid $1,500 or more in wages during any calendar quarter

- Had one or more employees work for at least 20 weeks

- Are subject to state unemployment tax laws

- Operate as a household employer or agricultural employer meeting specific thresholds

Important: Some exceptions apply for certain organizations. Professional tax services can determine your specific filing requirements.

Step-by-Step Guide to Completing Form 940

Step 1: Determine Your FUTA Liability

Calculate your FUTA tax obligation:

- First, $7,000 of each employee’s annual wages taxed at 6%

- Maximum credit reduction of 5.4% for state unemployment taxes paid

- The effective FUTA tax rate is typically 0.6% after credits

Step 2: Gather the Required Information

Prepare:

- Employee wage records for the year

- State unemployment tax payments

- Prior year Form 940 (if applicable)

- Quarterly financial statements showing payroll expenses

- EIN and business information

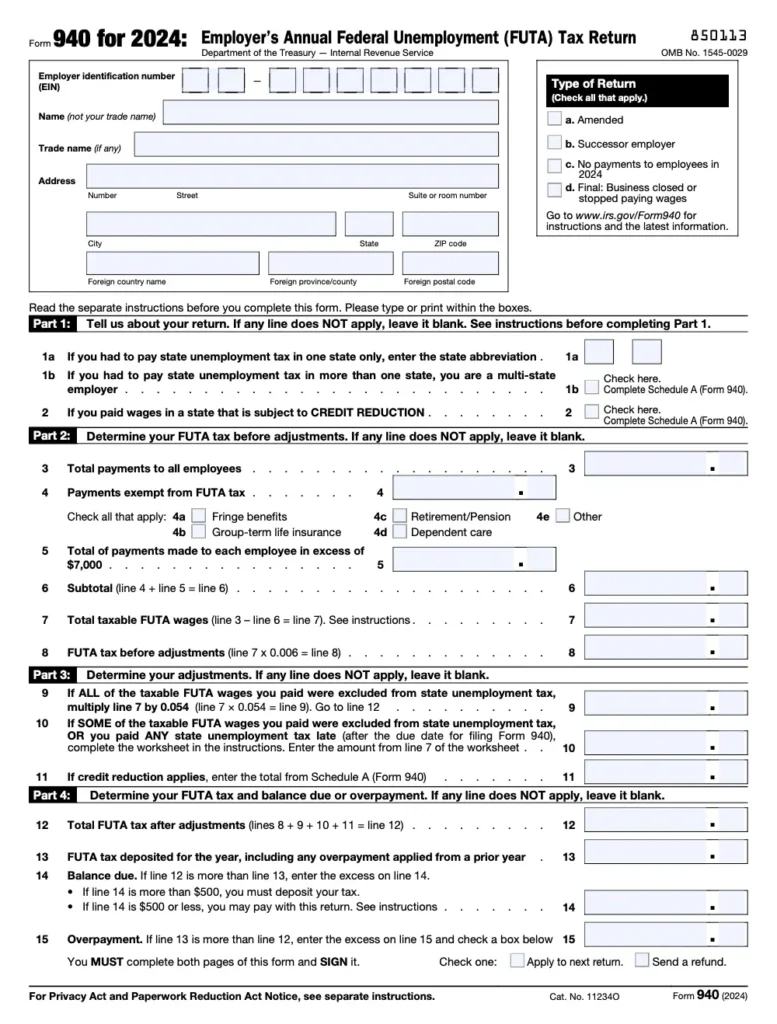

Step 3: Complete Part 1 – Employer Information

- Line 1: Legal business name

- Line 2: Employer Identification Number (EIN)

- Line 3: Trade name (if different)

- Line 4: Mailing address

- Line 5: State and ZIP code

Step 4: Complete Part 2 – Determine Your FUTA Tax

- Line 6: Total payments to employees

- Line 7: Exempt payments

- Line 8: Total taxable FUTA wages

- Line 9: Multiply Line 8 by 0.006

- Line 10: Credit reduction (if applicable)

Step 5: Complete Part 3 – Payments and Adjustments

- Line 11: Total FUTA tax after adjustments

- Line 12: Payments made during the year

- Line 13: Balance due or overpayment

Step 6: Complete Part 4 – State Unemployment Tax Information

- Line 14: Check if you’re a multi-state employer

- Line 15: List all states where you paid wages

- Line 16: Total state unemployment taxes paid

Step 7: Sign and File

- The authorized officer must sign and date

- File electronically through the IRS e-file system

Mail paper returns to:

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0046

- Deadline: January 31, following the tax year

Common Mistakes to Avoid

- Missing the filing deadline – Penalties apply for late filing

- Incorrect wage calculations – Only the first $7,000 per employee is taxable

- Miscalculating credits – Must adequately account for state unemployment taxes

- Failing to reconcile with financial statements – Must match payroll records

- Not maintaining proper documentation – Keep records for 4+ years

For businesses with complex payroll situations, professional tax services ensure accurate reporting.

Advanced Considerations

Financial Statement Reconciliation

- Align FUTA calculations with payroll records

- Track exempt vs. non-exempt wages

- Document credit reduction states

- Maintain audit trails for all calculations

Special Situations

- Agricultural employer rules

- Household employee requirements

- Successor employer situations

- Credit reduction states

State Compliance

- State unemployment tax rates

- Voluntary contribution options

- State-specific wage bases

- Combined reporting for multi-state employers

Final Thoughts

Proper completion of IRS Form 940 is essential for employers to meet their federal unemployment tax obligations. By maintaining accurate payroll records, reconciling with financial statements, and carefully following the latest Form 940 instructions, businesses can ensure compliance while adequately funding unemployment benefits. For employers with multi-state operations, seasonal workforce fluctuations, or complex payroll structures, partnering with professional tax services provides the expertise needed to navigate these requirements efficiently.