<!doctype html>

Net income serves as a key indicator of profitability for business owners and financial professionals. Understanding how to calculate it, what it includes, and how it connects to the rest of your financial statements is foundational to managing a healthy business.

Key Takeaways

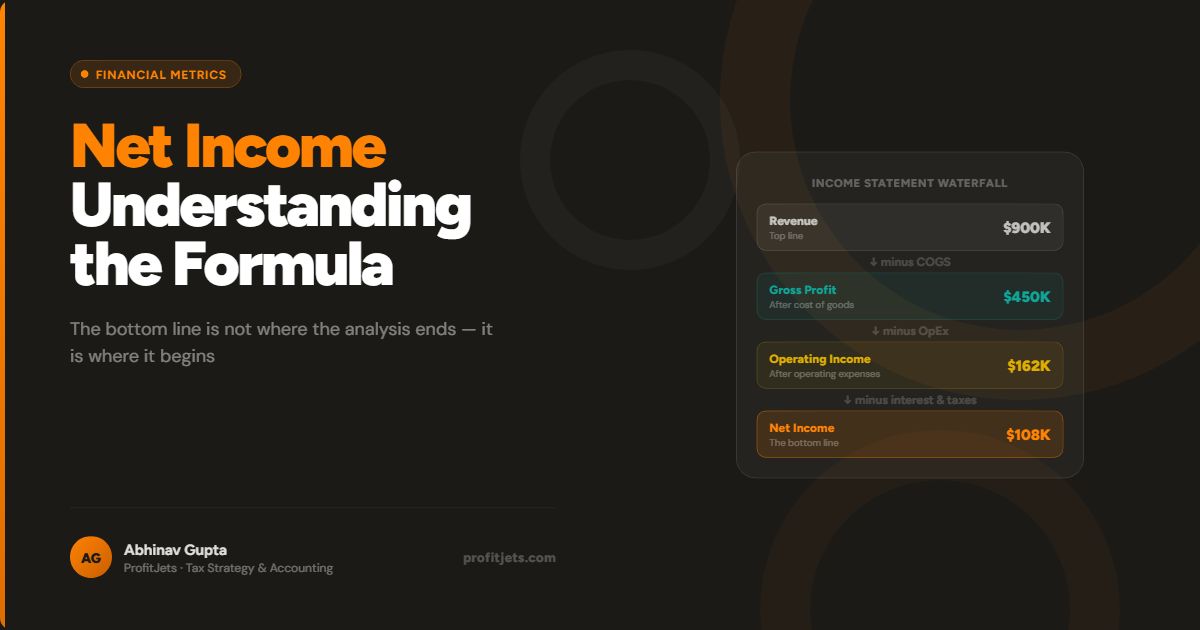

- Net income is calculated as: Total Revenue – Total Expenses. It is called the “bottom line” because it appears at the bottom of the income statement.

- Total expenses include operating costs, COGS, taxes and interest, and depreciation and amortization.

- Net income directly affects retained earnings on the balance sheet, linking the income statement to equity.

- Net income can be negative (a net loss) when total expenses exceed total revenue for the period.

For business owners and financial professionals, understanding how to calculate net income, what expenses feed into it, and how it connects to the rest of your financial statements is foundational to sound financial management.

What Is Net Income and Why Does It Matter?

Net income represents the amount remaining after all expenses have been subtracted from total revenue. It is the single figure that tells you whether your business made money or lost money during a specific period. That is why it appears at the very bottom of the income statement and is commonly called the “bottom line.”

Net income serves three primary purposes in financial management:

- Performance Analysis: It measures how efficiently a business converts revenue into profit after accounting for all costs.

- Investor Attraction: Investors and lenders use net income to assess whether a business is viable and worth funding.

- Tax Filing: Net income (adjusted for tax code provisions) forms the basis of your business tax return. Professional services help optimize deductions to minimize taxable income.

Net income is called the “bottom line” because it literally appears at the bottom of the income statement, after every category of expense has been subtracted from total revenue. A positive number means profit; a negative number means a net loss for the period.

The Formula and Calculation

The core net income formula is straightforward:

Applying this formula requires three steps:

- Determine Total Revenue. Add up all income your business earned during the period, including sales revenue, service fees, and any non-operating income such as investment returns.

- Calculate Total Expenses. Sum every cost the business incurred, including operating expenses, cost of goods sold, taxes, interest, and depreciation.

- Subtract Expenses from Revenue. The result is your net income (or net loss if expenses exceed revenue).

Worked Example

| Line Item | Amount |

|---|---|

| Total Revenue | $100,000 |

| Operating Expenses | ($40,000) |

| Taxes and Interest | ($10,000) |

| Net Income | $50,000 |

Expense Categories Included in Net Income

To calculate net income accurately, you need to account for every category of expense your business incurs. Missing even one category will overstate your profitability.

Operating Expenses

These are the day-to-day costs of running the business: rent, utilities, salaries and wages, insurance, and general administrative expenses. They are typically the largest expense category for service-based businesses.

Cost of Goods Sold (COGS)

COGS represents the direct costs of producing the goods or services you sell, including raw materials, direct labor, and manufacturing overhead. For product-based businesses, COGS is subtracted from revenue to arrive at gross profit before other operating expenses are applied.

Taxes and Interest

Income taxes owed to federal, state, and local governments, plus any interest expense on business loans or credit lines, are deducted in arriving at net income. These are often grouped together in smaller business income statements.

Depreciation and Amortization

These non-cash charges allocate the cost of long-lived assets (equipment, buildings, intangibles) over their useful lives. Even though no cash changes hands, depreciation and amortization reduce net income and are fully deductible for tax purposes.

Depreciation reduces net income on paper but does not reduce your cash balance. This is why some analysts look at EBITDA (earnings before interest, taxes, depreciation, and amortization) alongside net income to get a clearer picture of operating cash generation.

Gross Income vs. Net Income

These two terms are often confused, but they measure different things:

| Metric | What It Measures | Formula |

|---|---|---|

| Gross Income | Profitability of core production or service delivery | Revenue – COGS |

| Net Income | Overall financial health after all costs | Revenue – All Expenses |

Gross income focuses on production profitability and helps you understand whether your pricing covers your direct costs. Net income assesses the full picture, including operating overhead, taxes, and financing costs. Both metrics are needed for a complete analysis of business performance.

A business can have strong gross profit but near-zero or negative net income if operating expenses are high. This is a common signal that overhead costs, not production costs, are the main profitability problem and need to be addressed.

Connection to the Balance Sheet

Net income does not live only on the income statement. It flows directly into the equity section of the balance sheet through retained earnings.

At the end of each accounting period, net income is added to the beginning retained earnings balance (or net loss is subtracted from it). This retained earnings figure then appears on the balance sheet as part of stockholders’ equity or owners’ equity, linking what you earned this period to the cumulative history of the business.

Tax Importance of Net Income

Net income is the starting point for calculating your business tax liability. However, taxable income is not the same as accounting net income. Tax rules allow certain adjustments, deductions, and credits that can reduce the taxable figure below your book net income.

Professional tax services help you navigate these differences, ensuring that your financial records are complete, all allowable deductions are captured, and your tax filings comply with current regulations. Strategic tax planning around net income can meaningfully reduce your annual tax burden.

Want to reduce your taxable net income and keep more of what you earn?

Talk to a Tax ExpertThe Role of Professional Services

Calculating net income accurately requires reliable bookkeeping, clean categorization of expenses, and an understanding of which items belong on the income statement versus the balance sheet. Professional services make all of this faster, more accurate, and audit-ready.

- Bookkeeping Services: Ensure every transaction is recorded in the correct category, giving you a dependable net income figure at the end of each period.

- Tax Services: Translate accounting net income into taxable income using current IRS rules, maximizing deductions and minimizing liability.

- CFO Services: Provide strategic context for your net income trend, compare it to industry benchmarks, and advise on the operational changes that will move it in the right direction.

Frequently Asked Questions

What is the difference between operating income and net income?

Why is net income called the “bottom line”?

Can net income be negative?

What is the difference between gross income and net income?

How does net income affect the balance sheet?

Conclusion

Net income is more than just a number at the bottom of a report. It is the most complete measure of your business’s profitability, the figure that flows into your balance sheet, drives your tax filing, and tells investors whether your business is worth backing. Understanding the formula, the expense categories that feed into it, and how it connects to retained earnings gives you the foundation to make smarter financial decisions at every stage of business growth.

Need accurate net income reporting and strategic financial guidance?

Schedule a Free ConsultationProfitjets Editorial Team

The Profitjets team writes practical financial guides to help small and mid-sized business owners understand key metrics, improve cash flow, and make smarter decisions.