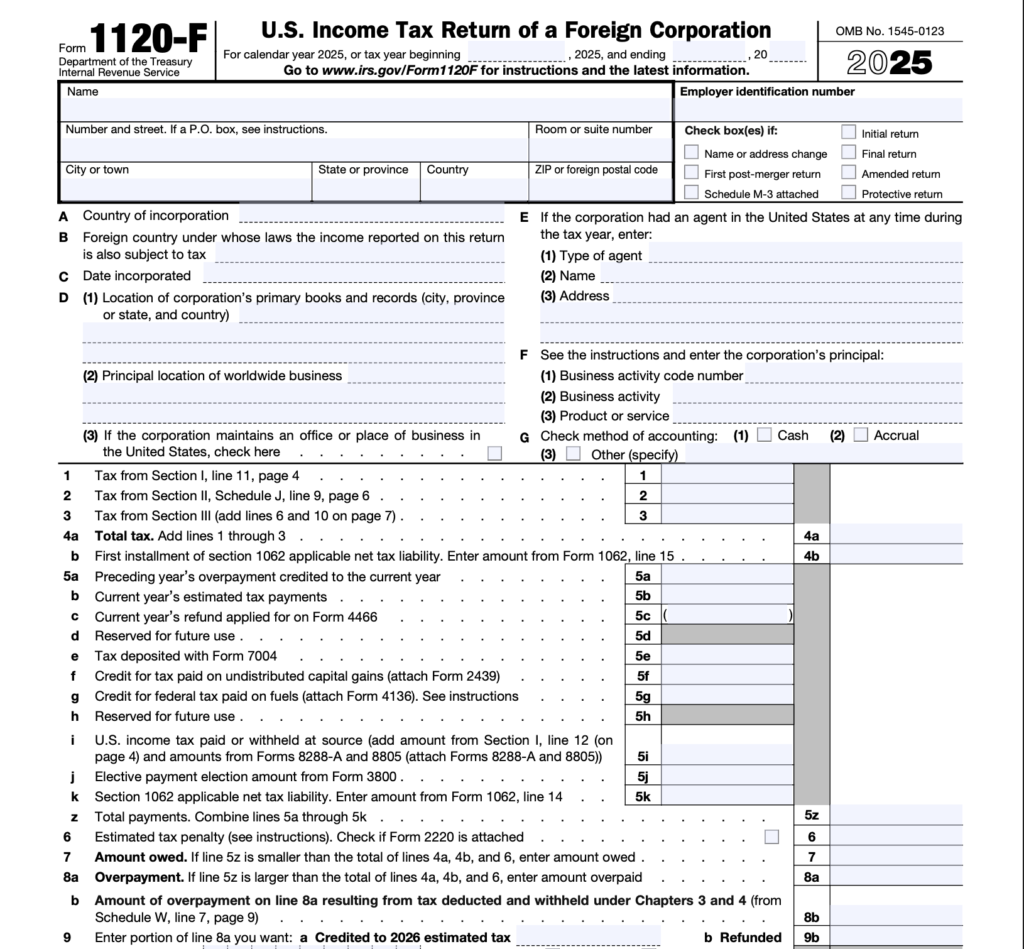

If you’re wondering what Form 1120-F is and whether it is an attachment to Form 1120, the answer is a big no. Form 1120-F is a separate tax return specifically for foreign (non-U.S.) corporations, not an add-on for domestic C corporation filings.

Foreign corporations that earn income from U.S. sources or engage in U.S. trade and business are required to file Form 1120-F to report their income and meet the regulatory obligations by the Internal Revenue Service.

Furthermore, proper filing ensures alignment with U.S. tax compliance requirements while supporting risk management, reporting accuracy, and cross-border tax efficiency.

What Is Form 1120-F in the US?

The U.S. Income Tax Return of a Foreign Corporation, or Form 1120-F, is used by foreign (non-US) corporations to report:

FDAP: Fixed, determinable, annual, or periodical income.

- Income effectively connected (ECI) with a U.S. trade or business

- U.S.-source income subject to withholding (FDAP)

- Applicable tax treaty positions

Unlike domestic corporations filing Form 1120, foreign entities must use Form 1120-F to disclose their U.S. business activities and tax obligations.

Key Definition:

“A foreign corporation is any company that is not incorporated or registered in the United States. This includes businesses formed in countries such as Canada, the UK, Germany, India, Japan, or any other non-U.S. jurisdiction.”

Who must file IRS Form 1120-F?

IRS Form 1120-F is required whenever a foreign corporation falls into any of the categories above during the tax year. The filing requirement of Form 1120-F is imposed by:

- Conducting any level of U.S. trade or business activity, which amounts to even a single transaction, can be enough in few circumstances.

- Receiving U.S.-source passive income that isn’t fully covered by withholding.

- Taking a position under a U.S. income tax treaty.

- Being required to report effectively connected income (ECI) or claiming deductions against ECI.

Important

“A foreign corporation with no U.S. income and no U.S. business activity during the year is generally not required to file. However, prior-year filing history and treaty claims may still create an obligation, so always confirm with a qualified international tax advisor.”

What Counts as Engaged in a U.S. Trade or Business?

The Internal Revenue Service (IRS) does not define “U.S. trade or business” with a single standardized rule, which is one of the most important aspects of Form 1120-F.

Generally, a foreign corporation is considered engaged in a U.S. trade or business if it has regular, continuous, and considerable activity in the U.S.

This can include:

- Maintaining a U.S. office, store, factory, or other fixed place of business.

- Having employees or dependent agents who perform services in the U.S.

- Performing personal services in the U.S.

- Trading in U.S. stocks, securities, or commodities through a U.S. office.

- Receiving income from U.S. real property (in certain elections).

Activities that generally do not qualify as a U.S. trade or business include:

- Trading stocks or securities for the corporation’s own account (under the “trading for own account” exemption in IRC §864(b)).

- Earning passive investment income, such as dividends or interest, without active involvement or management.

- Engaging in isolated or one-time transactions that lack continuity or regular business activity.

If there is any uncertainty about whether a specific activity constitutes a U.S. trade or business, please consult a qualified international tax advisor before making filing decisions.

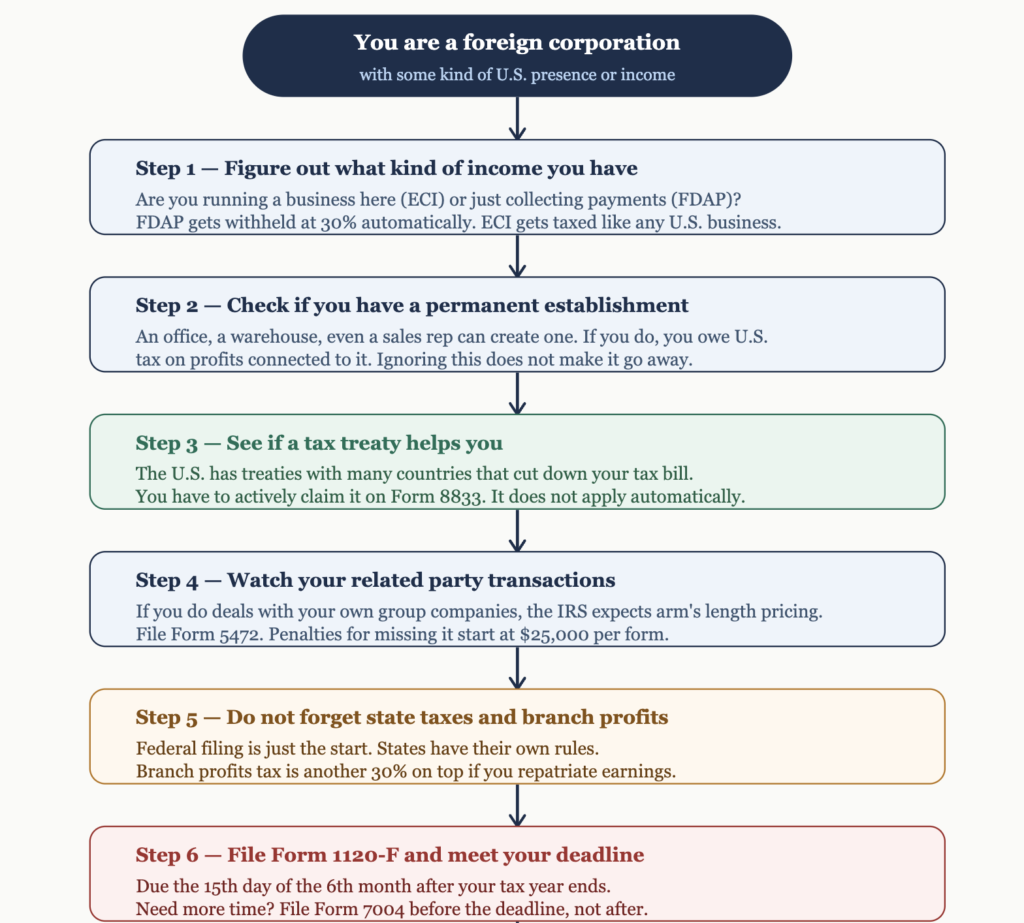

How to File Form 1120-F for Foreign Corporations (Step-by-Step)

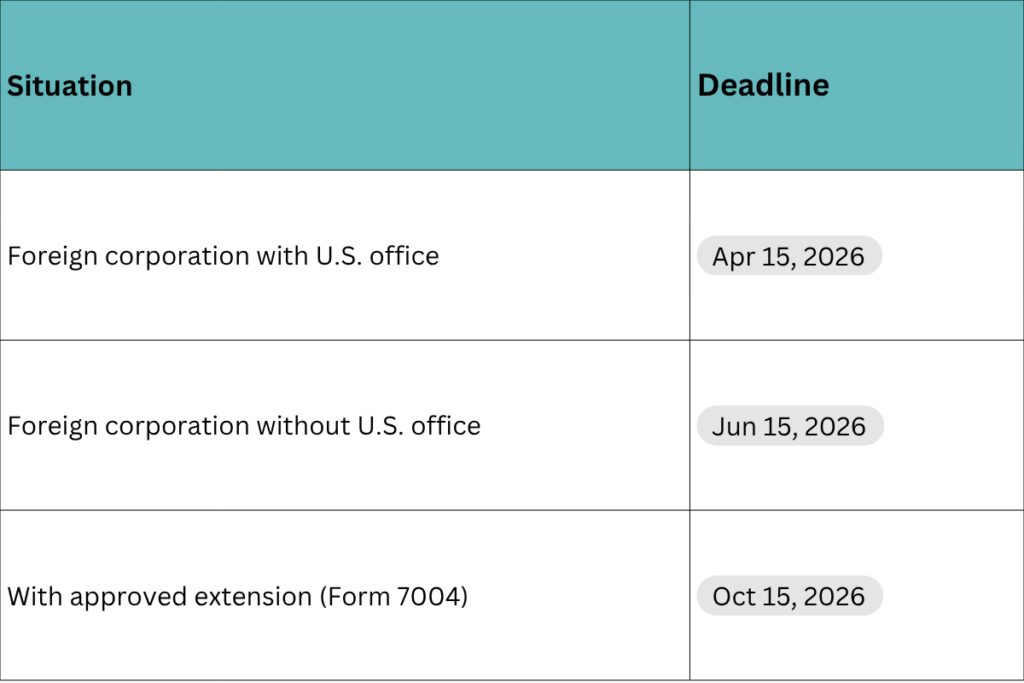

IRS Form 1120-F Deadlines for 2026

For a foreign corporation, meeting the correct deadline is required to preserve their deduction rights and avoid penalties.

Here are the key dates for the 2026 tax filing cycle (covering the 2025 tax year):

Key points to note:

- Foreign corporations that have a U.S. office or place of business follow the same April 15 deadline as domestic corporations.

- Those without a U.S. office are granted an automatic two-month extension to June 15, without needing to file a formal extension request.

- A further six-month extension can be obtained by filing Form 7004 before the original due date.

Deduction deadlines:

A foreign corporation that does not timely file or obtain an extension may permanently lose the right to claim deductions and credits against ECI for that tax year.

What are the Penalties If You Miss Filing Form 1120-F

The IRS takes non-compliance by foreign corporations seriously, and the penalties are structured to be particularly impactful:

Loss of deductions and credits

This is the most severe consequence. Under IRC Section 882(c)(2), if a foreign corporation does not file Form 1120-F within 18 months of the original due date, the IRS may disallow all deductions and credits against effectively connected income (ECI).

As a result, the corporation could be taxed on gross income instead of net income.

Monetary penalties

The IRS applies separate penalties for non-compliance:

Failure-to-file penalty: 5% of unpaid tax per month, up to 25%

Failure-to-pay penalty: 0.5% per month, up to 25%

If both apply, the total liability can increase significantly.

Interest charges

Interest is charged on any unpaid tax from the original due date until full payment is made. This is compounded daily at the federal short-term rate plus 3% interest.

Related-party reporting penalties

If Form 5472 is not filed or is incomplete, a penalty of $25,000 per form applies. Additional penalties may be imposed if the failure continues after IRS notification.

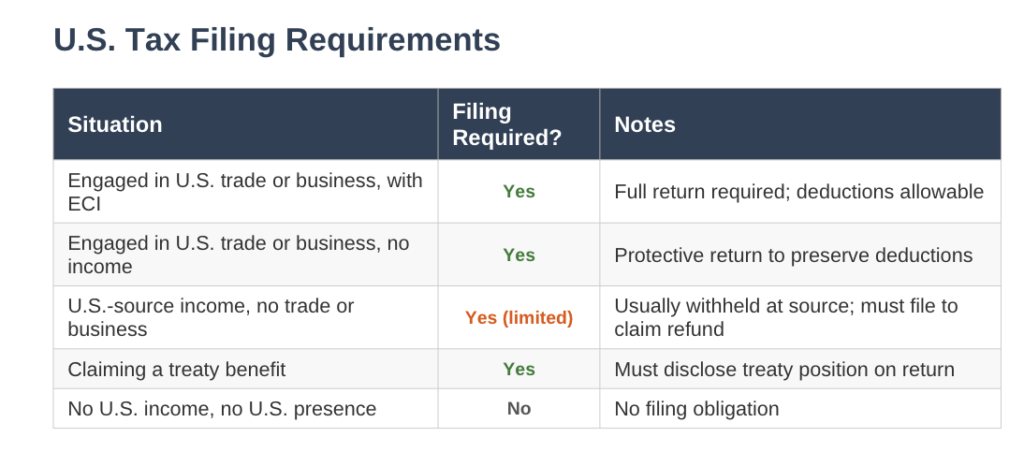

Things You Should Be Aware of Before Submitting Form 1120-F

Foreign corporations filing Form 1120-F should be mindful of several critical compliance factors that can directly impact tax liability and reporting obligations:

Here’s a quick reference flowchart for your reference:

Final check:

Ensure deadlines, disclosures, and related filings are reviewed before concluding no obligation.

How Profitjets Helps Foreign Corporations with Tax Filing

Filing Form 1120-F requires accurate income classification, proper treaty disclosure, and adherence to IRS compliance standards.

Given the complexity of cross-border taxation, even minor errors can lead to penalties or disallowed deductions.

Profitjets supports foreign corporations across the entire filing lifecycle, from EIN application and ECI classification to treaty reporting and final submission.

This ensures accuracy, reduces compliance risk, and helps maintain a structured, audit-ready approach to U.S. tax obligations.