Working capital is the money a business has available to run its day-to-day operations. It’s what’s left after subtracting current bills and expenses from current assets like cash and money owed by customers. In simple terms, it shows whether a business has enough cash to keep things running smoothly.

When you’re a small business owner, you pay your suppliers when the month starts. Your clients will pay you on the month end. The remaining 29-day gap left to gain your expense is where businesses quietly run out of money.

Whether you’re a startup trying to manage your expenses or a growing company planning your next expansion, understanding working capital management is essential. In this guide, we break down what working capital is, how to calculate it correctly, what the numbers actually mean, and most importantly how to improve it.

What Is Working Capital?

Working capital refers to the difference between a company’s current assets and its current liabilities. In simple terms, it tells you how much liquid money your business has available to cover its day-to-day operations.

Think of it as the financial breathing room your business needs to pay employees, restock inventory, handle unexpected expenses, and keep operations running, without reaching for a loan every month.

Working capital is a measure of short-term liquidity for businesses. It answers one direct question, If all your short-term obligations came due today, could you pay them?

If you want deeper financial structure and visibility, this is often supported through cash flow management services that ensure stability across operations.

Working Capital Formula for Business Growth

The working capital formula is used to calculate your assets and liabilities :

Working Capital = Current Assets − Current Liabilities

What Counts as Current Assets?

The Current assets are resources your business expects to convert into cash within 12 months:

- Cash and cash equivalents

- Accounts receivable (money owed to you by customers)

- Inventory

- Prepaid expenses

- Short-term investments

What Counts as Current Liabilities?

The Current liabilities are obligations due within 12 months:

- Accounts payable (money you owe suppliers)

- Short-term loans or lines of credit

- Accrued expenses (salaries, taxes, utilities)

- Current portion of long-term debt

Example Calculation

This business has $40,000 in working capital, meaning it can comfortably cover its short-term debts with room to spare.

How to Calculate the Working Capital Ratio

Working Capital Ratio = Current Assets ÷ Current Liabilities

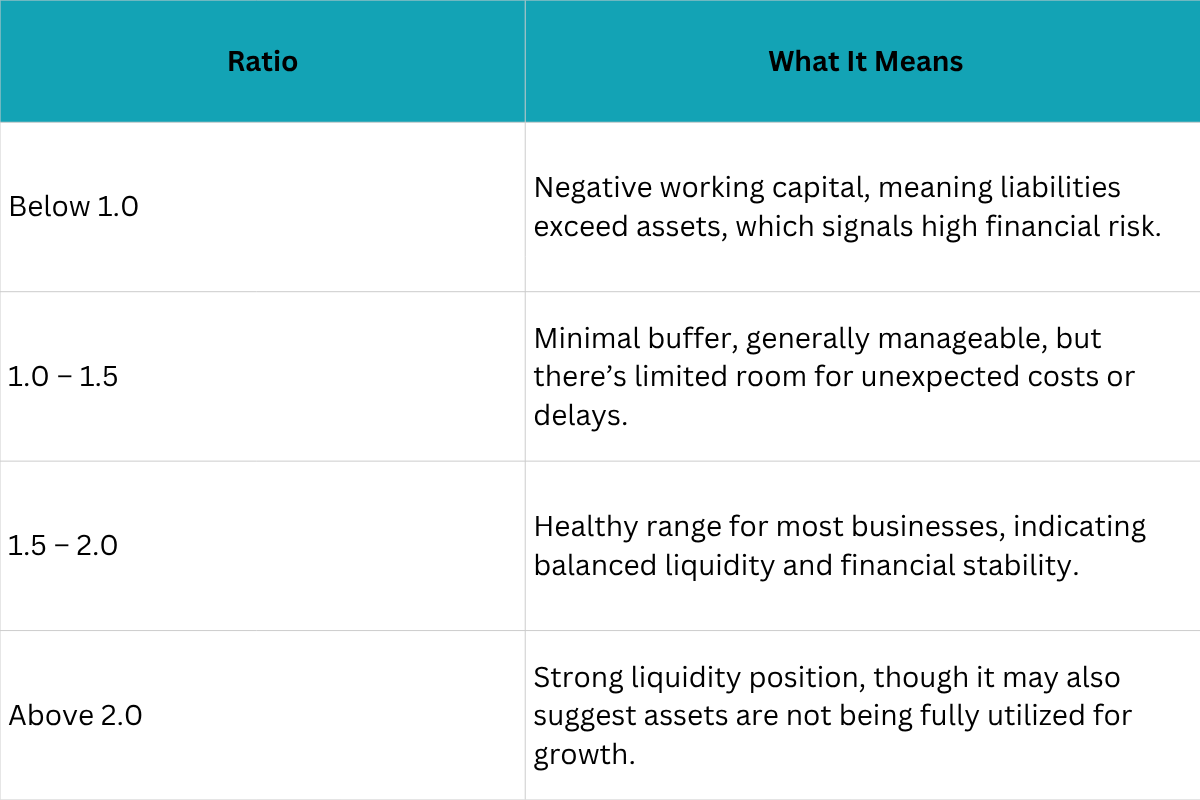

Using the example above: $100,000 ÷ $60,000 = 1.67

Here’s how to read the ratio:

Most lenders and investors consider a ratio between 1.5 and 2.0 to be the healthy working capital for your business. This metric is often tracked in financial reporting services to assess business stability.

Positive vs. Negative Working Capital: What’s the Difference?

Positive Working Capital

When current assets exceed current liabilities, your business has positive working capital. This means you can meet your short-term obligations, invest in growth opportunities, and absorb unexpected costs without relying on external financing.

Positive working capital signals financial stability to lenders, investors, and vendors.

Signs of Negative Working Capital

Negative working capital occurs when current liabilities exceed current assets. This doesn’t always mean a crisis, some industries like retail and restaurants operate this way intentionally because they collect cash before paying suppliers. However, for most businesses, it’s a red flag.

Warning signs of negative working capital include:

- Consistently missing vendor payment deadlines

- Relying on credit lines to cover payroll

- Declining cash reserves despite rising revenue

- Difficulty restocking inventory on time

- Customers or clients receiving delayed orders

If any of these sound familiar, your working capital cycle needs attention as fast as possible.

The Working Capital Cycle Explained

The working capital cycle which is also called the cash conversion cycle, is the time it takes for a business to convert its investments in inventory and other resources into cash through sales.

Working Capital Cycle = Days Inventory Outstanding + Days Sales Outstanding − Days Payable Outstanding

A shorter cycle means your business recovers cash faster. A longer cycle means cash stays tied up for longer, increasing your financing needs.

Example:

- You purchase inventory: Day 0

- Inventory sits in the warehouse: 20 days

- You sell and invoice a customer: Day 20

- Customer pays: Day 50

- You pay your supplier: Day 40

Your cash was tied up for 50 days but you paid your supplier on day 40, creating a 10-day gap you need to finance. This is where effective working capital management for small businesses becomes critical.

7 Proven Strategies to Improve Working Capital

Here are the proven ways to improve your working capital for long term growth.

1. Speed Up Accounts Receivable Collections

Every day a customer holds your invoice is a day you don’t have that cash. To optimize accounts receivable and improve cash flow:

- Offer early payment discounts (e.g., 2% off if paid within 10 days)

- Send invoices immediately after delivery

- Automate payment reminders

- Review your credit terms and check if the payment terms really necessary.

2. Extend Accounts Payable (Without Damaging Relationships)

On the other hand, try negotiating longer payment terms with your suppliers whenever possible. Extending terms from net-30 to net-45 or net-60 helps you keep cash in your business for a longer period. Just make sure this doesn’t hurt your vendor relationships or cause you to miss out on valuable early payment discounts.

3. Optimize Your Inventory Management

Dead inventory drains cash. Overstocking ties up money that could be deployed elsewhere. Use demand forecasting to order smarter, run periodic audits to clear slow-moving stock, and consider just-in-time (JIT) inventory practices for eligible product lines.

4. Secure a Business Line of Credit, Before You Need It

A revolving line of credit is one of the most practical tools for managing short-term cash shortfalls. Apply when your finances are strong, not when you’re already in trouble. This gives you a safety net without the pressure of emergency borrowing terms.

5. Cut Unnecessary Short-Term Liabilities

Review every recurring expense under 12 months. Are there subscriptions, contracts, or retainers that aren’t delivering value? Eliminating unnecessary current liabilities directly improves your working capital position.

6. Convert Short-Term Debt to Long-Term Financing

If a portion of your debt is short-term but relates to long-term assets (like equipment or real estate), explore refinancing it as long-term debt. This removes it from current liabilities, improving your working capital ratio.

7. Improve Cash Flow Forecasting

Many businesses don’t have a cash flow problem, they have a visibility problem. By forecasting cash inflows and outflows on a weekly or monthly basis, you can spot gaps before they become crises and make smarter decisions about timing expenses and collections.

Common Working Capital Mistakes Businesses Make

Even financially savvy business owners fall into these traps:

❌ Confusing profit with cash flow

Your income statement might show strong profit, but if that revenue is sitting in unpaid invoices, you could still be cash-strapped. Working capital lives in cash flow reality, not accounting theory.

❌ Ignoring seasonal fluctuations

Businesses with seasonal revenue peaks often underestimate how low working capital can drop in off-months. Planning for these cycles in advance is essential.

❌ Letting receivables age unchecked

Invoices that age beyond 90 days often become uncollectable. Establish a collections process before that happens.

❌ Over-investing in fixed assets

Buying equipment or property with cash that should be working capital is a common mistake. Use financing for long-term assets; preserve cash for operations.

Main Takeaway

Most business owners think about working capital only when there’s a problem. But the businesses that grow sustainably treat it as something to actively manage, measure, and optimize every quarter.

Positive working capital gives you the freedom to take on new clients, negotiate better vendor terms, invest in talent, and scale without constantly worrying about making payroll. Negative working capital, left unaddressed, can derail even a profitable business.

How Profitjets Helps You Manage Working Capital

Understanding the numbers is one thing. Acting on them is another.

At Profitjets, we work with business owners to go beyond basic bookkeeping and into the metrics that actually drive decisions. Our team helps you:

- Build accurate cash flow forecasts

- Identify working capital leaks in your receivables and payables cycle

- Set up financial dashboards that give you real-time visibility

- Align your short-term liquidity management with your long-term growth strategy

The result? You stop flying blind and start making confident, data-backed financial decisions.

The formula to manage it consistently is where most businesses fall short and where a trusted financial partner makes all the difference.

Frequently Asked Questions

What is working capital and why does it matter for my business?

Working capital is the money left after subtracting your short-term bills from your short-term assets. It matters because it shows whether your business can pay employees, restock inventory, and handle daily expenses without reaching for a loan every month.

How do you calculate working capital?

Use this simple formula: Working Capital = Current Assets − Current Liabilities If your current assets are $100,000 and liabilities are $60,000, your working capital is $40,000, meaning you have a healthy buffer to cover short-term obligations.

What is a healthy working capital ratio for a small business?

A ratio between 1.5 and 2.0 is considered ideal by most lenders and investors. Below 1.0 is a warning sign. Above 2.0 may suggest you’re not investing your excess cash efficiently enough.

What causes negative working capital and how do I fix it?

Negative working capital happens when your bills exceed your available assets often due to slow-paying customers, overstocked inventory, or heavy short-term debt. You can fix it by speeding up invoice collections, negotiating longer supplier payment terms, and cutting unnecessary short-term expenses.

What is the difference between working capital and cash flow?

Working capital is a point-in-time snapshot of your short-term financial health. Cash flow tracks money moving in and out over time. A business can show strong profit on paper but still struggle with working capital if revenue is stuck in unpaid invoices