Your Days Sales Outstanding is a direct report of how effectively your business converts revenue into usable cash. Businesses that monitor DSO consistently are better positioned to protect liquidity, strengthen working capital, and avoid preventable cash flow pressure as they grow.

Businesses can show strong sales and healthy profits on paper while still struggling to cover payroll, suppliers, or day-to-day operations because the cash has not been collected.

Many small business owners, monitor revenue growth and profit margins closely, yet overlook DSO until liquidity strain forces attention on collections. By that stage, receivables aging and liquidity strain have often been building quietly for months.

This guide breaks down what DSO actually means for your business, how to calculate it correctly, what good looks like by industry, and most importantly what levers you can pull today to bring it down.

What Is DSO in Accounting

Days Sales Outstanding (DSO) is a financial metric that measures the average number of days it takes your business to collect payment after a sale has been made. It is a core accounting metric recognized by the AICPA and widely used in financial reporting frameworks including GAAP-compliant working capital analysis.

DSO directly determines how long cash stays tied up in receivables before it’s available to fund operations, pay staff, or reinvest in growth. The IRS guidelines for small business financial reporting emphasizes accurate receivables tracking and recordkeeping for businesses help leverage cash flow and reporting obligations.

In plain terms, DSO tells you how long your money sits in someone else’s account after you’ve already done the work.

- A DSO of 30 means you’re collecting within your invoice terms and capital is cycling efficiently.

- A DSO of 75 means your customers are taking two and a half months to pay. Every extra day past your terms is a day your operating capital is frozen.

DSO is a core component of the cash conversion cycle (CCC), the full journey of cash from operations, through sales, and back into your account. Managing DSO is one of the highest-leverage actions any business owner can take to strengthen working capital without touching a single expense line.

How to Calculate Days Sales Outstanding(DSO)

The standard DSO formula is calculated by,

DSO = (Accounts Receivable ÷ Total Credit Sales) × Number of Days

Most businesses calculate DSO on a monthly (30 days) or quarterly (90 days) basis. Quarterly gives a more stable picture and smooths out month-to-month fluctuation.

DSO Calculation with Example

A B2B consulting firm ends Q1 with:

- Accounts receivable balance: $120,000

- Total credit sales for the quarter: $360,000

DSO = ($120,000 ÷ $360,000) × 90 = 30 days

The DSO ratio of 30 days signs healthy. Collections are cycling roughly every 30 days, which aligns with standard net-30 payment terms.

Now, when we run the same calculation six months later with same revenue, but receivables have climbed:

- Accounts receivable balance: $210,000

- Total credit sales for the quarter: $360,000 (unchanged)

DSO = ($210,000 ÷ $360,000) × 90 = 52.5 days

Same revenue and same terms. Receivables up 75%. Cash cycle stretched by three weeks. The income statement didn’t change but cash availability dropped sharply. That is exactly how financially healthy businesses end up in cash flow trouble.

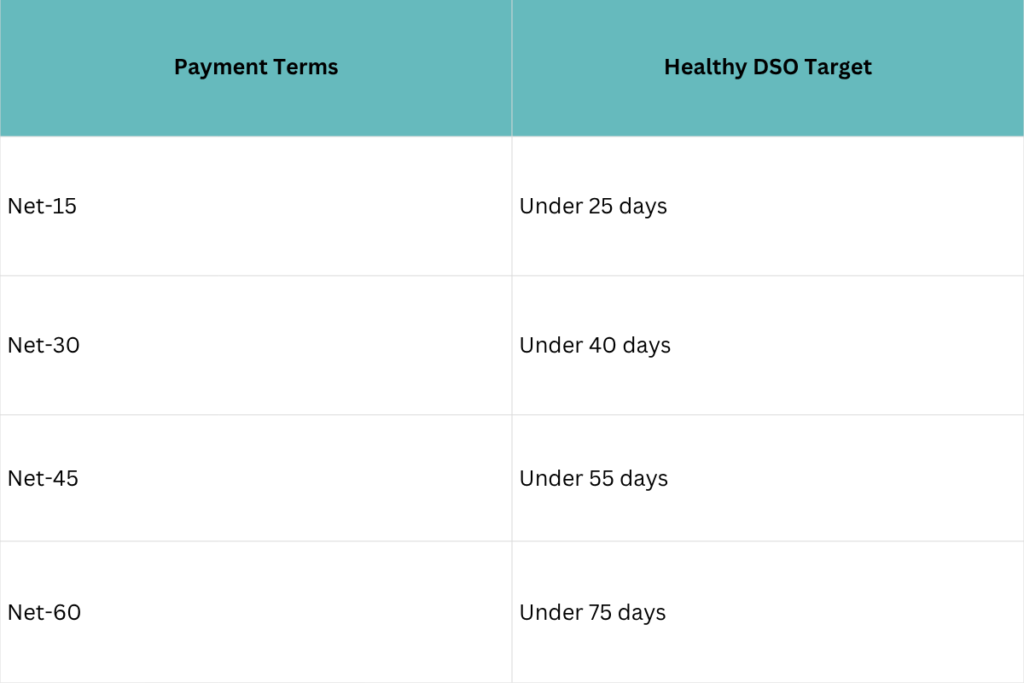

What Is a Healthy DSO Ratio for Your Business

A healthy DSO ratio depends on your payment terms, customer behavior, and industry operating model. However, the following ranges provide a practical benchmark for most businesses:

As a general rule, when DSO exceeds 1.5× your standard payment terms, it usually signals weaknesses in collections, invoicing processes, or customer payment discipline.

Days Sales Outstanding Benchmarks by Industry

DSO expectations vary significantly across industries due to billing structures and payment cycles:

- B2B Professional Services (consulting, legal, and marketing): Typically 35–50 days due to project-based invoicing and approval cycles.

- Government Contractors: Often 45–60 days, as extended payment timelines are built into the operating model.

- SaaS & Subscription Businesses: Can range from near-zero with card-on-file billing to much higher for enterprise invoicing models.

- Wholesale & Distribution: Commonly 30–50 days depending on customer concentration and credit terms.

- Healthcare & Medical Practices: Frequently above 40 days due to insurance reimbursement timelines.

If your DSO has increased from 35 days to 58 days over the past year under the same payment terms, it signals a deterioration in cash conversion efficiency regardless of what competitors are experiencing.

Why High DSO Is a Cash Flow Crisis

Here’s the insight that most business owners miss: a rising DSO doesn’t show up as a problem on your income statement.

Revenue is recognized at the point of sale, not at collection. A business can post three consecutive quarters of strong revenue growth while its actual cash position deteriorates steadily because collections are lagging further and further behind.

This is precisely how profitable businesses end up struggling to fund payroll. The revenue is real, but the cash just isn’t there. For growing businesses, the problem compounds. Higher revenue generates more receivables.

If DSO is climbing simultaneously, the dollars tied up in outstanding invoices scale with the business. A company growing 30% year-over-year with DSO expanding from 35 to 55 days may find that growth actually worsens the cash position before it improves it

How to Reduce DSO: Six Practical Steps That Work

1. Send Invoice Immediately After Delivering the Product or Service

Every delay between delivery and invoicing extends your cash conversion cycle and postpones when revenue becomes usable cash. Invoicing at project completion rather than at month-end alone often reduces DSO by 5 to 10 days without any other changes.

2. Tighten Payment Terms for New Customers

Net-30 is not an obligation. Many businesses move new accounts to net-15 and reserve extended terms for established relationships with a clean payment history. Shorter terms lower your DSO ceiling structurally.

3. Strategise Early Payment Incentives

A 1–2% discount for payment within 10 days is a proven method for accelerating collections. The cost of the discount is typically far below the cost of carrying the receivable especially when you factor in credit line interest or the opportunity cost of constrained cash.

4. Automate Your Collections Reminder Sequence

A structured reminder process, a courtesy note 7 days before due, a firm reminder on the due date, an escalation at 15 days past consistently outperforms manual follow-up. The critical factor is consistency. Manual processes break down under operational load but automation doesn’t.

5. Move to Weekly Aging Report Reviews

Most businesses review accounts receivable monthly at best. Weekly reviews catch problems earlier. An invoice at 25 days overdue is far more collectible than one at 65 days. Aging reports should be a standing weekly agenda item, not an occasional finance task.

6. Build a 48-Hour Dispute Resolution Process

Billing disputes that sit unresolved for two or three weeks inflate DSO and damage client relationships simultaneously. A defined process for identifying and resolving disputes within 48 hours of escalation removes one of the most common but underappreciated drivers of receivables aging.

The Hidden Costs of High DSO That Rarely Show Up on Financial Reports

Here are the hidden costs of elevated days sales outstanding that you need to be aware of for informed desicion making:

Financing Costs

When collections slow down, many businesses rely on credit lines or short-term borrowing to cover day-to-day operations. The interest paid on that financing becomes a direct cost of elevated DSO.

For example, carrying $500,000 in receivables that remain unpaid 20 days beyond terms at a 7% borrowing rate creates a measurable financing burden, one that stronger collections processes could often eliminate entirely.

Increased Bad Debt Risk

Invoices that age beyond 90 days are at a higher risk of becoming uncollectable. The longer a receivable sits, the harder it is to collect. Businesses with usually high DSO that don’t monitor aging closely often discover that a portion of their current assets are aging receivables.This means the balance sheet accuracy is compromised and current assets include receivables that will never convert to cash, overstating the actual financial position.

Operational Limitations

Cash tied up in receivables cannot be deployed elsewhere in the business. It restricts hiring decisions, delays inventory purchases, slows expansion initiatives, and limits operational flexibility. In many cases, businesses postpone growth opportunities not because revenue is weak, but because cash collection is lagging behind sales.

How Profitjets Helps You Turn Receivables Into Cash Faster

Tracking DSO is easy once you have accurate, current accounts receivable data. Acting on it requires a system: clean records, aging reports that update regularly, and financial visibility that lets you catch problems before they affect operations.

If your receivables are growing faster than your cash balance, it may be time to review your collections process and working capital strategy. At Profitjets, we help business owners build the reporting infrastructure that makes these metrics actionable. That means reconciled receivables, weekly aging reports, and CFO-level analysis that connects your DSO to your broader cash flow position, so you’re not discovering a collections problem the month you need the cash.

If your receivables aren’t being managed as actively as your revenue,

Frequently Asked Questions (FAQs)

What causes DSO to increase even when revenue is growing?

Revenue growth does not automatically improve cash flow. In many businesses, rapid growth increases receivables faster than collections capacity. Extended payment terms, delayed invoicing, weak follow-up processes, or customer concentration can all push DSO higher even during strong sales periods.

How does a high DSO affect cash flow and working capital?

A high DSO delays the conversion of revenue into usable cash, reducing available working capital for payroll, inventory, operations, and growth investments. Businesses with elevated DSO often rely more heavily on credit lines or short-term financing to bridge cash flow gaps.

What is the difference between DSO and accounts receivable turnover?

DSO measures the average number of days it takes to collect payment after a sale, while accounts receivable turnover measures how many times receivables are collected during a period. Both evaluate collection efficiency, but DSO provides a clearer cash flow timing perspective for operational decision-making.

Why do investors and lenders monitor DSO closely?

Investors and lenders view DSO as an indicator of liquidity quality and operational discipline. Rising DSO may signal weakening collections, customer payment risk, or deteriorating working capital efficiency even when reported revenue and profits appear strong.

How often should businesses review DSO and receivables aging reports?

Businesses should monitor DSO monthly at minimum, while receivables aging reports should ideally be reviewed weekly. Frequent monitoring helps identify slow-paying accounts early, reduce bad debt exposure, and prevent small collection delays from turning into larger liquidity issues.