If you’ve ever sat across from a bookkeeper or reviewed a financial report and quietly nodded while having no idea what half the terms meant, you’re not alone. And you’re not behind. Here’s the truth about accounting: most small business owners don’t need to become accountants. But they do need to understand what their accountant is telling them. Accounting has its own language, and nobody hands you a dictionary when you start a business.

This guide does exactly that. We’ve broken down 15 of the most important accounting terms for 2026, so you can read your financials with confidence, ask better questions, and make smarter decisions, whether you’re running a startup, a freelance practice, or an eCommerce brand.

Table of Contents

- Why Accounting Literacy Matters in 2026

- 15 Accounting Terms Every Business Owner Should Know

- Bonus: 2026 Accounting Terms Worth Adding to Your Vocabulary

- How Outsourced Accounting Services Help You Use These Terms

- Frequently Asked Questions

Why Accounting Literacy Matters in 2026

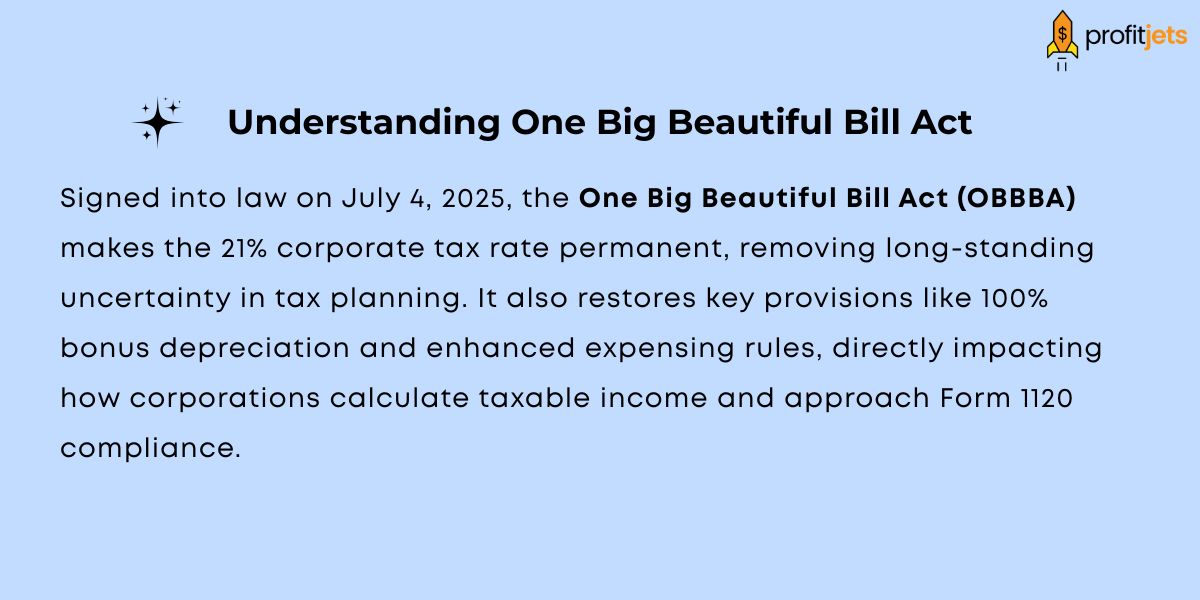

The accounting landscape in 2026 isn’t static. Between the FASB rolling out new standards, the IRS updating inflation-adjusted thresholds under the One Big Beautiful Bill Act (OBBBA), and expanded reporting requirements for tips and overtime, there’s more reason than ever to stay informed.

You don’t need to master all of it. But knowing the foundational terms puts you in a position to actually engage with your numbers, catch errors early, and stop making decisions based on vibes instead of data.

That’s what this guide is for. Let’s get into it.

15 Accounting Terms Every Business Owner Should Know

1. Accountant

An accountant is a trained financial professional responsible for recording, analyzing, and reporting your business’s transactions. A Certified Public Accountant (CPA) is licensed by the state and held to specific professional standards, they can represent you before the IRS, conduct audits, and sign off on financial statements. Not every accountant is a CPA, and not every bookkeeper is an accountant, so understanding the difference matters when you’re deciding who to hire.

2. Accountant’s Report

This is a document prepared by an accountant that summarizes a review, compilation, or attestation of your financial statements. It’s not the same as a full audit as it provides a level of financial assurance without the full audit opinion. Lenders, investors, and some grant programs may require one, so it’s worth knowing what you’re being asked for before you commit.

3. Accounts Payable (AP)

Accounts payable is everything your business owes to vendors, suppliers, and service providers in simple terms money going out. It sits on your balance sheet as a liability, which means it directly reduces your equity. If your accounts payable AP is growing faster than your revenue, that’s a cash flow warning sign worth paying attention to.

4. Accounts Receivable (AR)

The flip side of AP accounts receivable is money owed to your business by customers or clients for work already done or products already delivered. It’s recorded as an asset, but it’s only real money once it’s collected. Tracking AR closely is one of the most underrated cash flow habits a small business can build.

5. Accounting Period

An accounting period is the specific timeframe your financial reporting covers: monthly, quarterly, or annually. This is the window your income statement, cash flow statement, and other reports are measured against. It matters for tax filings, investor reporting, and internal performance tracking. Most U.S. businesses use the calendar year (January–December), but a fiscal year ending on a different date is also permitted by the IRS.

6. Accrual

In accounting, an accrual is the recognition of revenue or expense before cash actually changes hands. If you completed a project in December but get paid in January, under accrual accounting, that revenue belongs to December which is the period when it was earned. The IRS requires businesses with average annual gross receipts exceeding $32 million (adjusted annually for inflation, per IRC §448) to use the accrual method. Below that threshold, most small businesses can choose.

7. Accrued Expenses

Accrued expenses are costs your business has incurred but hasn’t yet paid , think unpaid wages at month-end, utility bills not yet invoiced, or interest accumulating on a loan. Recording them accurately is essential because they affect both your profit and your tax liability. Skipping them leads to overstated earnings and an incomplete picture of what you actually owe.

8. Balance Sheet

The balance sheet is a snapshot of your business’s financial position at a single point in time. It’s built around one equation that never changes:

Assets are what you own. Liabilities are what you owe. Equity is what’s left over for you. If a lender, investor, or potential buyer asks to see your financials, the balance sheet is typically the first document they look at.

9. Capital

Capital refers to the financial resources available to fund and grow your business.

Working capital is the money you have to nurture and scale your business

A positive working capital means you can cover your short-term obligations. A negative working capital is a signal that the business is living paycheck to paycheck.

10. Cash Basis Accounting

Under cash basis accounting, income is recorded when cash is received and expenses are recorded when cash is paid. No invoice dates, no earned/incurred logic. It’s the simpler of the two main accounting methods and is used by most small service businesses in the U.S. The IRS permits cash basis accounting as long as your three-year average gross receipts stay below the inflation-adjusted threshold (currently $32 million for 2026). Once you cross it, accrual is required.

11. Cash Flow

Cash flow is the movement of money in and out of your business over a specific period. Positive cash flow means more is coming in than going out. Negative cash flow means the opposite and it’s one of the primary reasons businesses fail, even profitable ones. Profit and cash flow are not the same thing. A business can show accounting profit while running out of actual cash, which is why tracking both separately is so important.

12. Cost of Goods Sold (COGS)

COGS is the direct cost of producing the products or services you sell: materials, direct labor, manufacturing overhead. It does not include operating expenses like rent or marketing. The formula is simple:

Gross Profit = Revenue − COGS

Understanding your COGS is essential for pricing correctly. If you don’t know what it costs to produce what you sell, you can’t know whether you’re actually making money on it.

13. Diversification

In a business accounting context, diversification refers to spreading revenue streams, investments, or business activities across multiple areas to reduce risk. A business that relies on a single client for 80% of its revenue isn’t diversified and that concentration shows up as financial vulnerability when you look at it through an accounting lens. It’s a term that crosses over into financial planning and business strategy, but it starts with understanding your revenue breakdown.

14. Dividends

Dividends are distributions of profit paid to the owners or shareholders of a business. They come out of retained earnings, which means paying dividends reduces the equity on your balance sheet. For S-corps and partnerships, distributions work similarly. Understanding how dividends and distributions are classified matters for both accounting accuracy and tax treatment ,they’re handled differently than salary, and the IRS pays close attention to the distinction.

15. Double-Entry Bookkeeping

Double-entry bookkeeping is the accounting system where every financial transaction is recorded in at least two accounts, one debit and one credit, so that the books always balance. It’s been the foundation of modern accounting since the 15th century, and it’s the reason your balance sheet equation always holds. Every accounting software platform in use today runs on double-entry logic, even if you never see the debits and credits directly.

Additional Accounting Terms Worth Adding to Your Vocabulary

The core 15 terms above are timeless. But 2026 brings a few additions worth knowing, particularly if you’re scaling or navigating new compliance requirements.

GAAP (Generally Accepted Accounting Principles)

The standardized framework governing how U.S. companies report financial information, developed and maintained by the Financial Accounting Standards Board (FASB). Private small businesses aren’t legally required to follow GAAP, but banks and investors often expect it when you’re seeking financing or going through due diligence. FASB continues to update standards regularly , 2026 brings new disclosure requirements for public companies that may eventually trickle down to private reporting expectations.

QBI Deduction (Qualified Business Income)

A significant tax benefit for pass-through business owners (sole proprietors, S-corps, partnerships). Under the OBBBA, the phase-in income ranges expanded in 2026, meaning some pass-through owners who didn’t previously qualify may now be eligible for up to a 20% deduction on qualified business income. This is an accounting term with a real dollar impact, worth a direct conversation with your CPA.

EBITDA

EBITDA is Earnings Before Interest, Taxes, Depreciation, and Amortization. A widely used measure of operating performance that strips out financing and accounting decisions to show raw business profitability. If you’re ever in a valuation conversation, a lender review, or a potential acquisition, someone will bring up your EBITDA.

Burn Rate

Relevant especially for startups: the rate at which your business is spending its cash reserves. Monthly burn rate divided into your available cash gives you your “runway” of how many months you have before you need new revenue or additional funding.

ACH Payments

Automated Clearing House transfers are a digital payment method widely used for payroll, vendor payments, and recurring billing. From an accounting standpoint, ACH transactions need to be reconciled the same way checks do but they’re faster, cheaper, and significantly lower fraud risk than paper checks.

How Outsourced Accounting Services Help You Use These Terms

Knowing these terms is a great start. But understanding them in the context of your business’s actual numbers that’s where outsourced accounting earns its value.

A good outsourced accounting partner doesn’t just keep your books. They translate what the numbers mean, flag issues before they become problems, and make sure your financial reporting reflects what’s actually happening in your business not just what happened three months ago.

For small businesses, startups, and eCommerce brands, outsourcing accounting typically costs a fraction of what an in-house hire would run. You get access to professionals who stay current on IRS changes, GAAP updates, and accounting standards without the overhead of salary, benefits, and training.

At Profitjets, our outsourced bookkeeping and accounting services are built around the specific needs of U.S. small businesses. From monthly bookkeeping and reconciliation to financial reporting and tax-ready accounting, we make sure your numbers are accurate, accessible, and actually useful for decision-making.

Knowing your accounting terms is just the beginning.

Frequently Asked Questions

What’s the difference between accounting and bookkeeping?

Bookkeeping is the day-to-day recording of financial transactions: invoices, receipts, payments. Accounting is the broader discipline that includes analyzing those records, preparing financial statements, and using the data to guide business decisions. Most businesses need both, and they often overlap, especially with outsourced services.

What’s the difference between accounts payable and accounts receivable?

Accounts payable is what your business owes to others: vendor bills, supplier invoices. Accounts receivable is what others owe your business — client invoices that haven’t been paid yet. Managing both well is essential for healthy cash flow.

Should I use cash basis or accrual accounting?

For most small service businesses in the U.S., cash basis is simpler and perfectly legal. Accrual accounting gives you a more accurate picture of financial performance and is required by the IRS once your three-year average gross receipts exceed $32 million. If you’re seeking bank financing or planning to sell your business, lenders and buyers typically prefer accrual-basis financials. When in doubt, ask your CPA.

How often should I review my balance sheet?

Monthly is the standard for most businesses. Reviewing it quarterly at minimum ensures you catch issues: growing liabilities, shrinking equity, receivables that aren’t converting to cash before they become serious problems.

What’s the importance of double-entry bookkeeping?

It keeps your books balanced and auditable. Every transaction has two sides, which means errors are caught faster and financial statements are more reliable. It’s also the foundation of every accounting software platform in use today.

Can a small business benefit from outsourced accounting services?

Yes, and for most small businesses, it’s more cost-effective than hiring in-house. Outsourced accounting gives you access to expertise, software, and compliance knowledge without the overhead. It also frees up your time to focus on running the business, not managing spreadsheets.